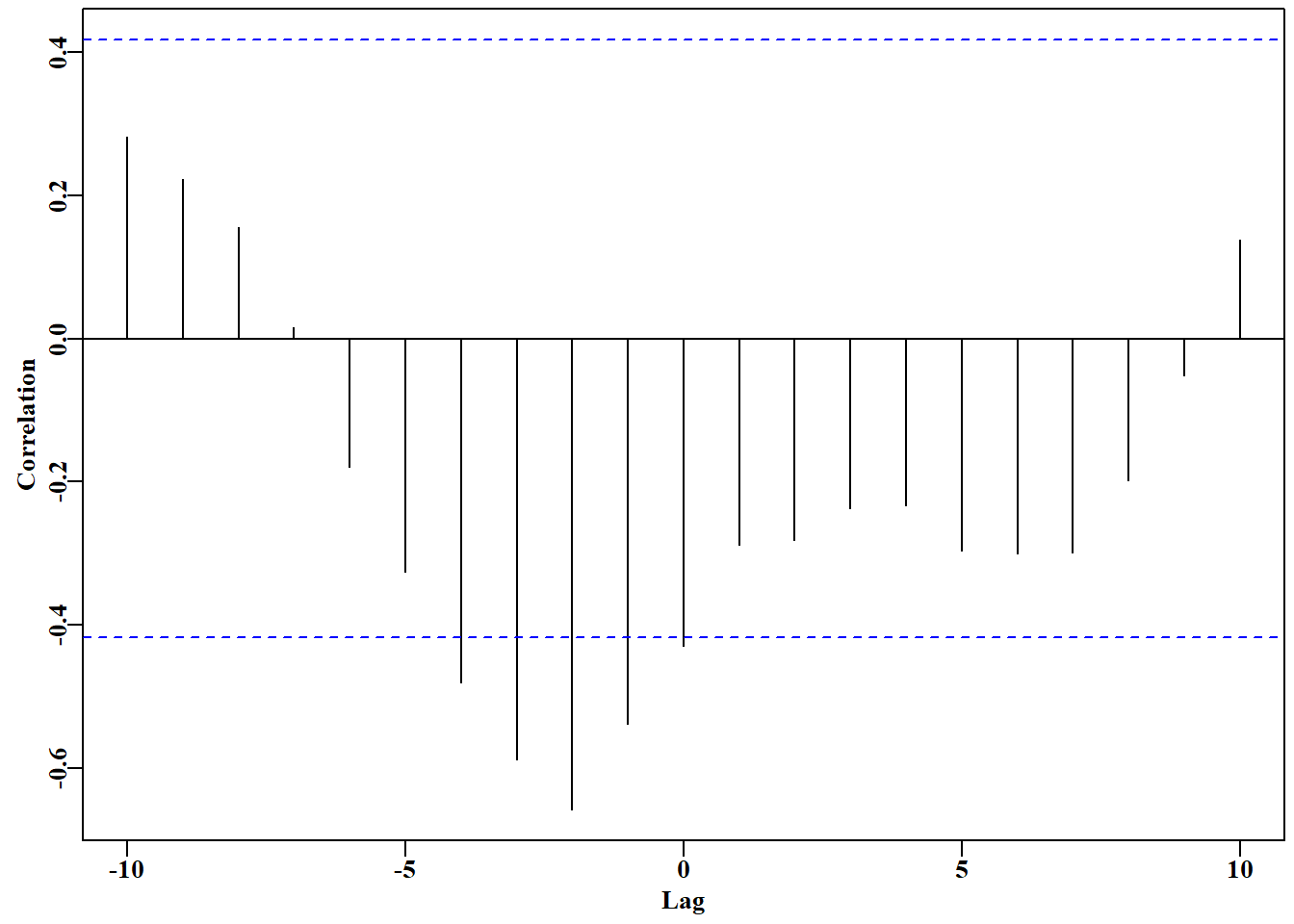

# cross correlation between cpue and catch in schaef Fig 7.2parset(cex =0.85)# sets par parameters for a tidy base graphicccf( x =schaef[, "catch"], y =schaef[, "cpue"], type ="correlation", ylab ="Correlation", plot =TRUE)

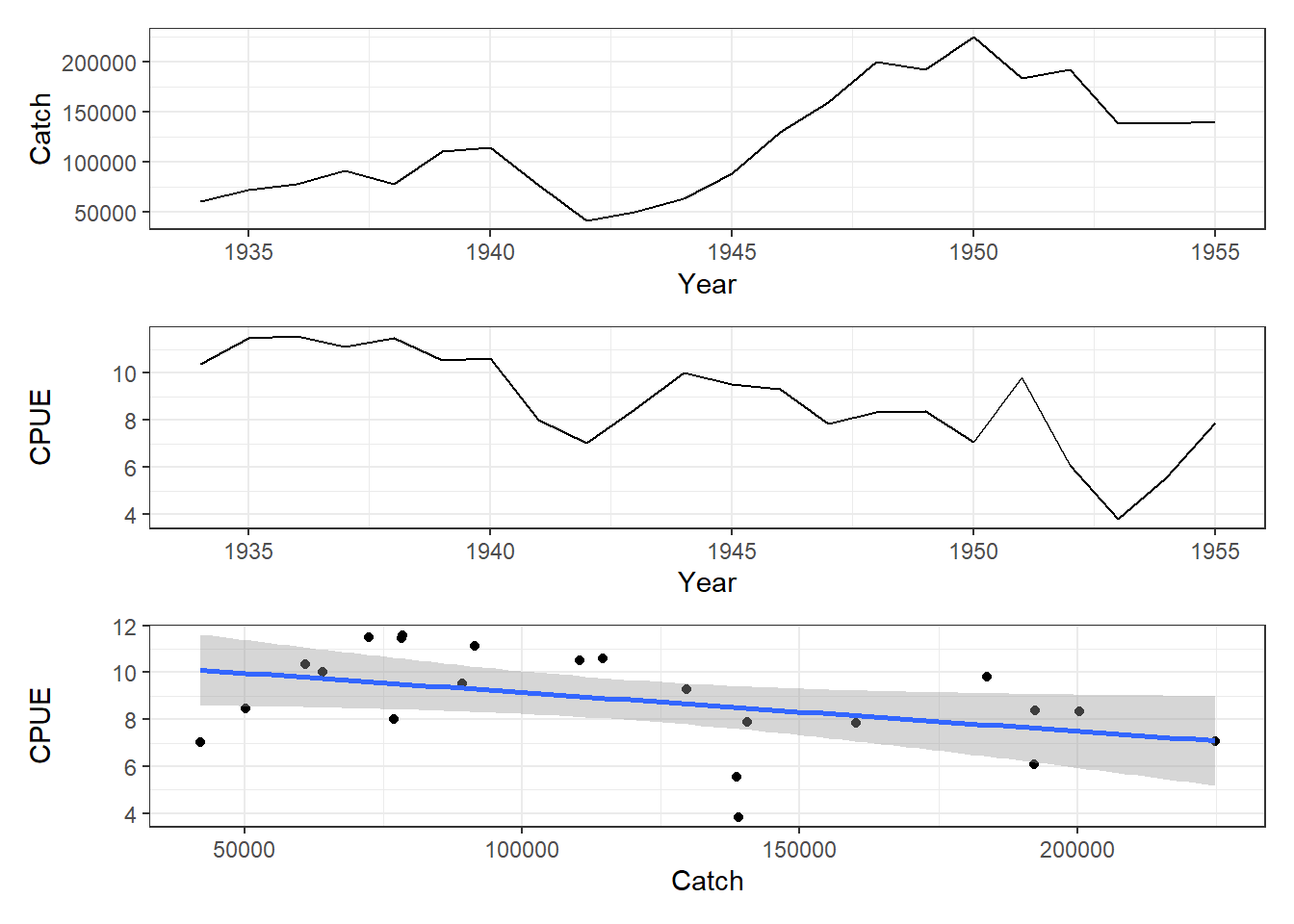

# now plot schaef data with timelag of 2 years on cpue Fig 7.3model2<-lm(schaef[3:22, "cpue"]~schaef[1:20, "catch"])# parset(plots=c(3,1),margin=c(0.35,0.4,0.05,0.05))# plot1(schaef[1:20,"year"],schaef[1:20,"catch"],ylab="Catch",# xlab="Year",defpar=FALSE,lwd=2)# plot1(schaef[3:22,"year"],schaef[3:22,"cpue"],ylab="CPUE",# xlab="Year",defpar=FALSE,lwd=2)# plot(schaef[1:20,"catch"],schaef[3:22,"cpue"],type="p",# ylab="CPUE",xlab="Catch",defpar=FALSE,cex=1.0,pch=16)## abline(model2,lwd=2,col=2)p1<-schaef|>filter(year<=1953)|>ggplot(aes(x =year, y =catch))+geom_line()+theme_bw()p2<-schaef|>filter(year>1935)|>ggplot(aes(x =year, y =cpue))+geom_line()+theme_bw()l<-nrow(schaef)schaef1<-data.frame( catch =schaef[1:(l-2), "catch"], cpue =schaef[3:l, "cpue"])p3<-ggplot(data =schaef1, aes(x =catch, y =cpue))+geom_point()+geom_smooth(method ="lm")+theme_bw()p1/p2/p3

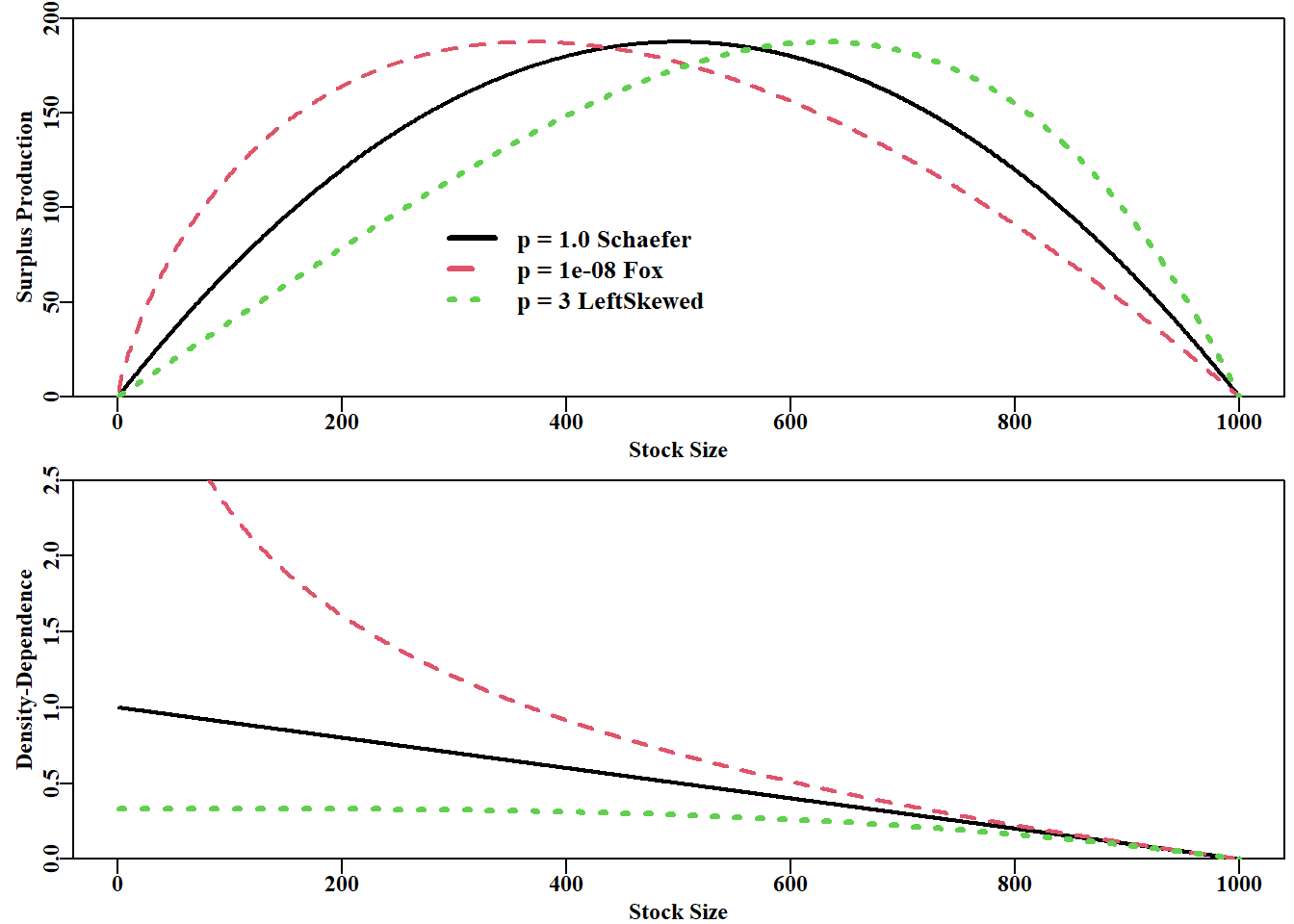

# compare Schaefer and Fox MSY estimates for same parametersparam<-c(r =1.1, K =1000.0, Binit =800.0, sigma =0.075)cat("MSY Schaefer = ", getMSY(param, p =1.0), "\n")# p=1 is default

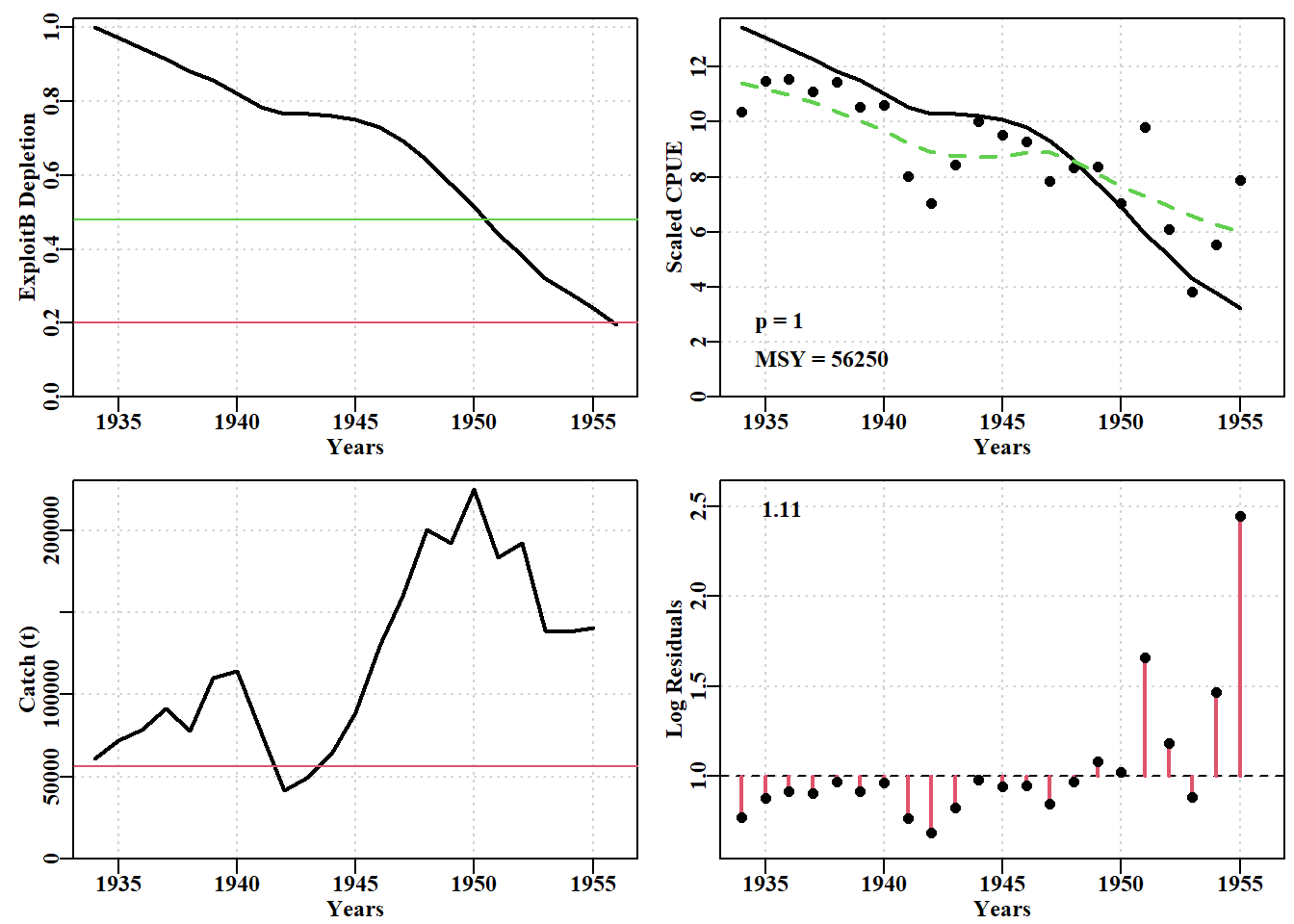

# Fit the model first using optim then nlm in sequenceparam<-log(c(0.1, 2250000, 2250000, 0.5))pnams<-c("r", "K", "Binit", "sigma")best<-optim( par =param, fn =negLL, funk =simpspm, indat =schaef, logobs =log(schaef[, "cpue"]), method ="BFGS")outfit(best, digits =4, title ="Optim", parnames =pnams)

# the high-level structure of ans; try str(ans$Dynamics)str(ans, width =65, strict.width ="cut", max.level =1)

List of 12

$ Dynamics :List of 5

$ BiomProd : num [1:200, 1:2] 100 10687 21273 31860 42446 ...

..- attr(*, "dimnames")=List of 2

$ rmseresid: num 1.03

$ MSY : num 123731

$ Bmsy : num 1048169

$ Dmsy : num 0.498

$ Blim : num 423562

$ Btarg : num 1016409

$ Ctarg : num 123581

$ Dcurr : Named num 0.528

..- attr(*, "names")= chr "1956"

$ rmse :List of 1

$ sigma : num 0.169

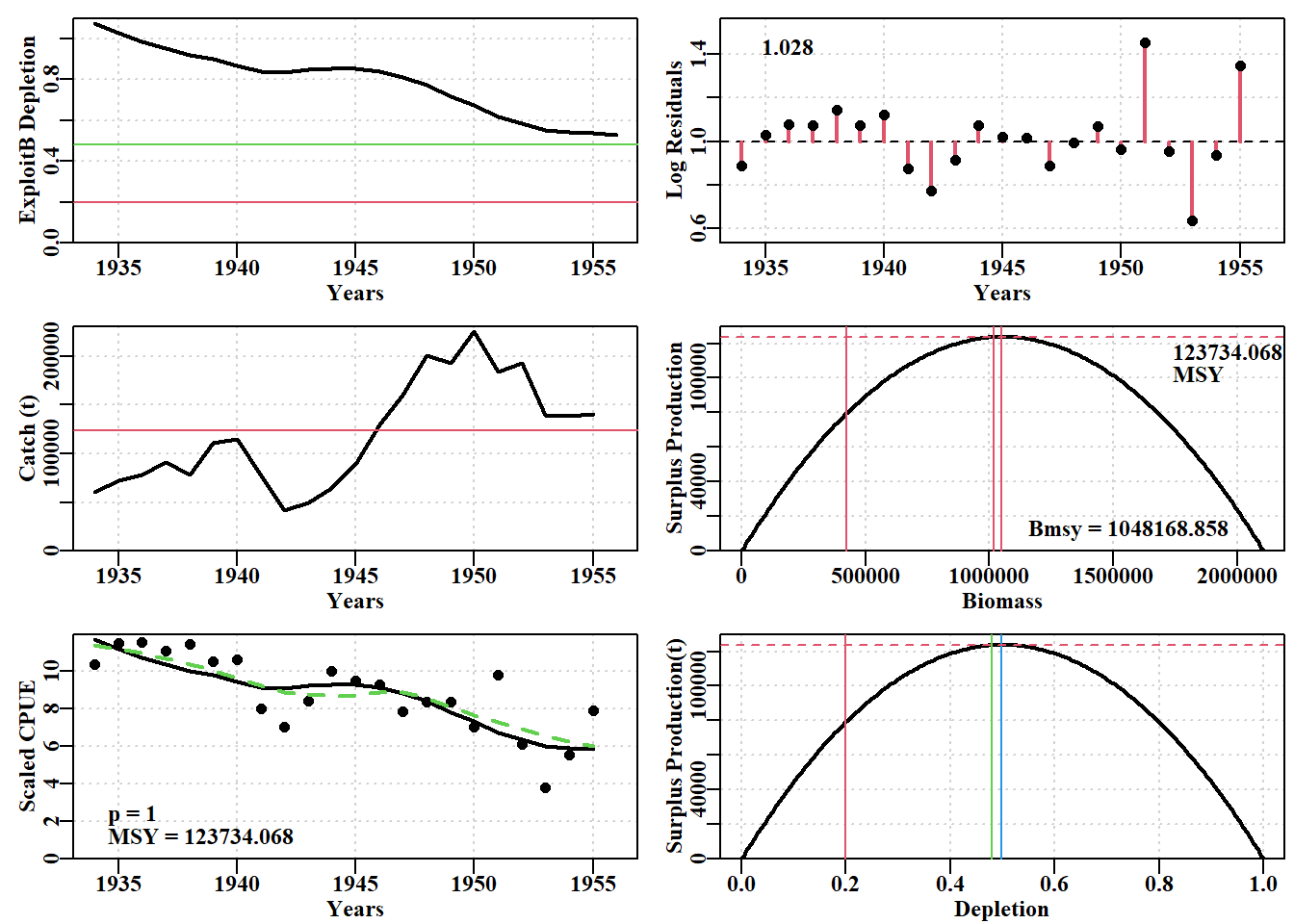

# conduct a robustness test on the Schaefer model fitdata(schaef)schaef<-as.matrix(schaef)reps<-12param<-log(c(r =0.15, K =2250000, Binit =2250000, sigma =0.5))ansS<-fitSPM( pars =param, fish =schaef, schaefer =TRUE, # use maxiter =1000, funk =simpspm, funkone =FALSE)# fitSPM# getseed() #generates random seed for repeatable resultsset.seed(777852)# sets random number generator with a known seedrobout<-robustSPM( inpar =ansS$estimate, fish =schaef, N =reps, scaler =40, verbose =FALSE, schaefer =TRUE, funk =simpspm, funkone =FALSE)# use str(robout) to see the components included in the output

表 7.2: A robustness test of the fit to the schaef data-set. By examining the results object we can see the individual variation. The top columns relate to the initial parameters and the bottom columns, perhaps of more interest, to the model fits.

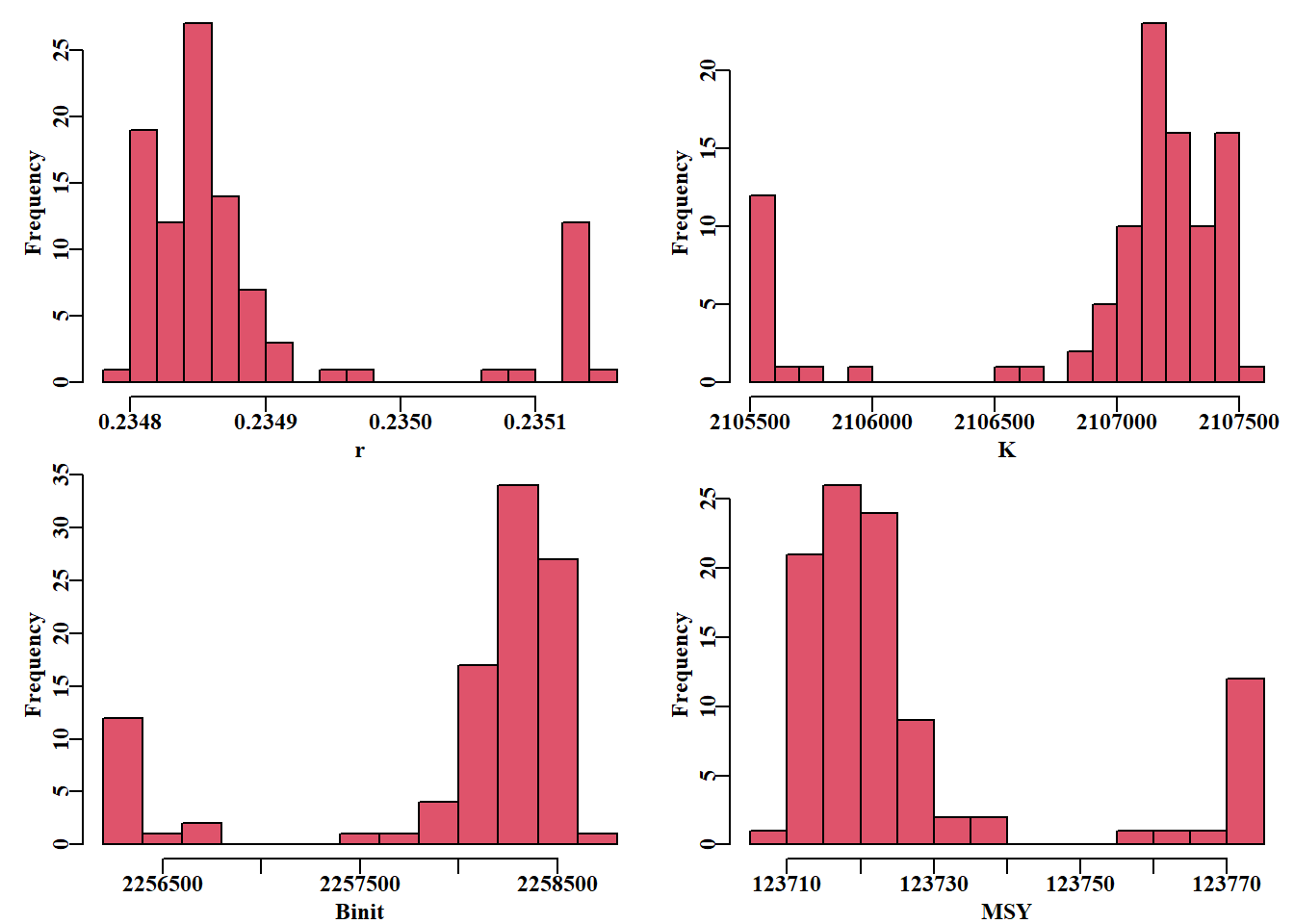

# Repeat robustness test on fit to schaef data 100 timesset.seed(777854)robout2<-robustSPM( inpar =ansS$estimate, fish =schaef, N =100, scaler =25, verbose =FALSE, schaefer =TRUE, funk =simpspm, funkone =TRUE, steptol =1e-06)lastbits<-tail(robout2$results[, 6:11], 10)

表 7.3: The last 10 trials from the 100 illustrating that the last three trials deviated a little from the optimum negative log-likelihood of -7.93406.

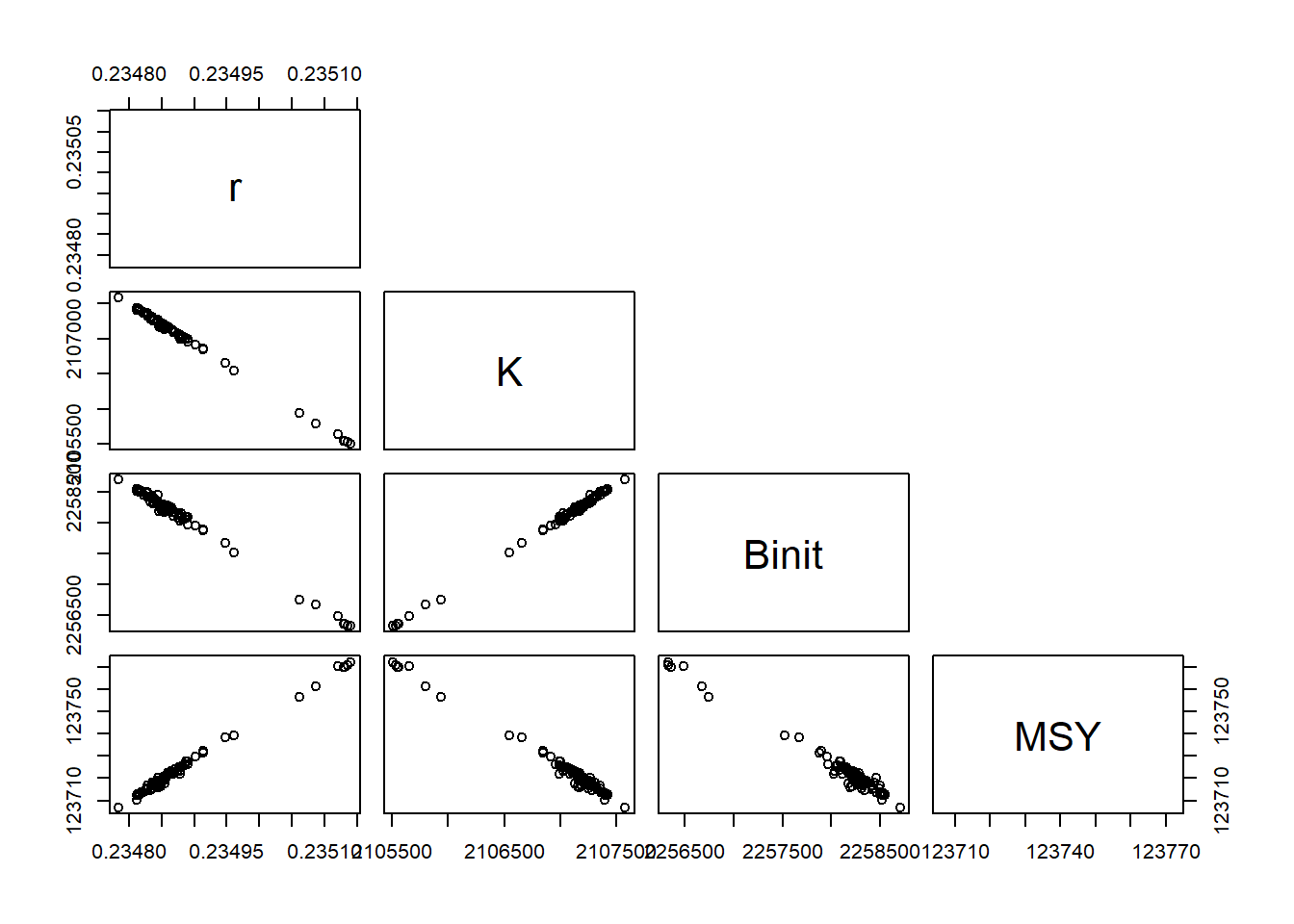

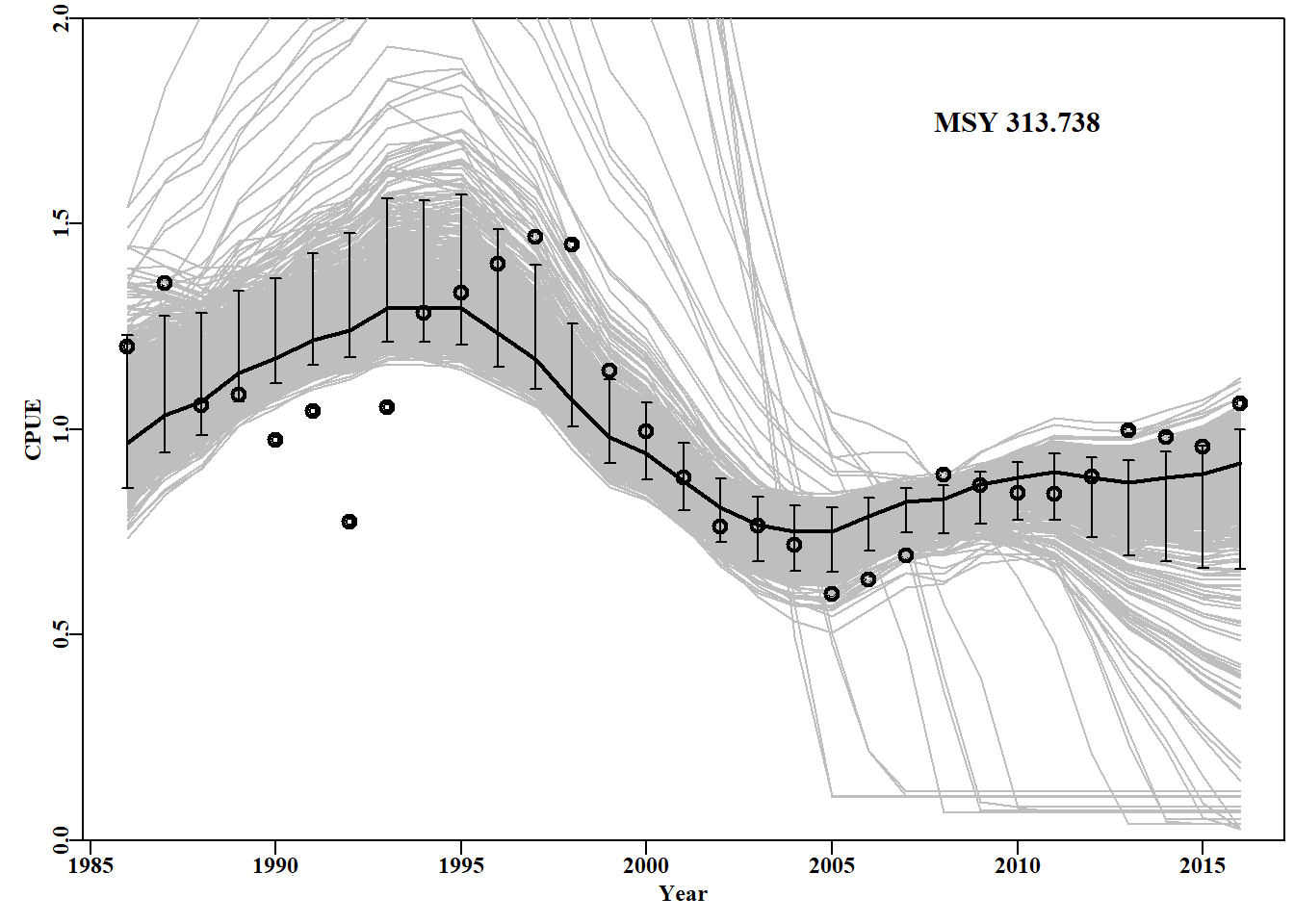

# replicates from the robustness test Fig 7.7result<-robout2$resultsparset(plots =c(2, 2), margin =c(0.35, 0.45, 0.05, 0.05))hist(result[, "r"], breaks =15, col =2, main ="", xlab ="r")hist(result[, "K"], breaks =15, col =2, main ="", xlab ="K")hist(result[, "Binit"], breaks =15, col =2, main ="", xlab ="Binit")hist(result[, "MSY"], breaks =15, col =2, main ="", xlab ="MSY")

# Now use the dataspm data-set, which is noisierset.seed(777854)# other random seeds give different resultsdata(dataspm)fish<-dataspm# to generalize the codeparam<-log(c(r =0.24, K =5174, Binit =2846, sigma =0.164))ans<-fitSPM( pars =param, fish =fish, schaefer =TRUE, maxiter =1000, funkone =TRUE)out<-robustSPM(ans$estimate, fish, N =100, scaler =15, # making verbose =FALSE, funkone =TRUE)# scaler=10 givesresult<-tail(out$results[, 6:11], 10)# 16 sub-optimal results

表 7.4: The last 10 trials from 100 used with dataspm. The last six trials deviate markedly from the optimum negative log-likelihood of -12.1288, and five gave consistent sub-optimal optima. Variation across parameter estimates with the optimum log-likelihood remained minor, but was large for the false optima.

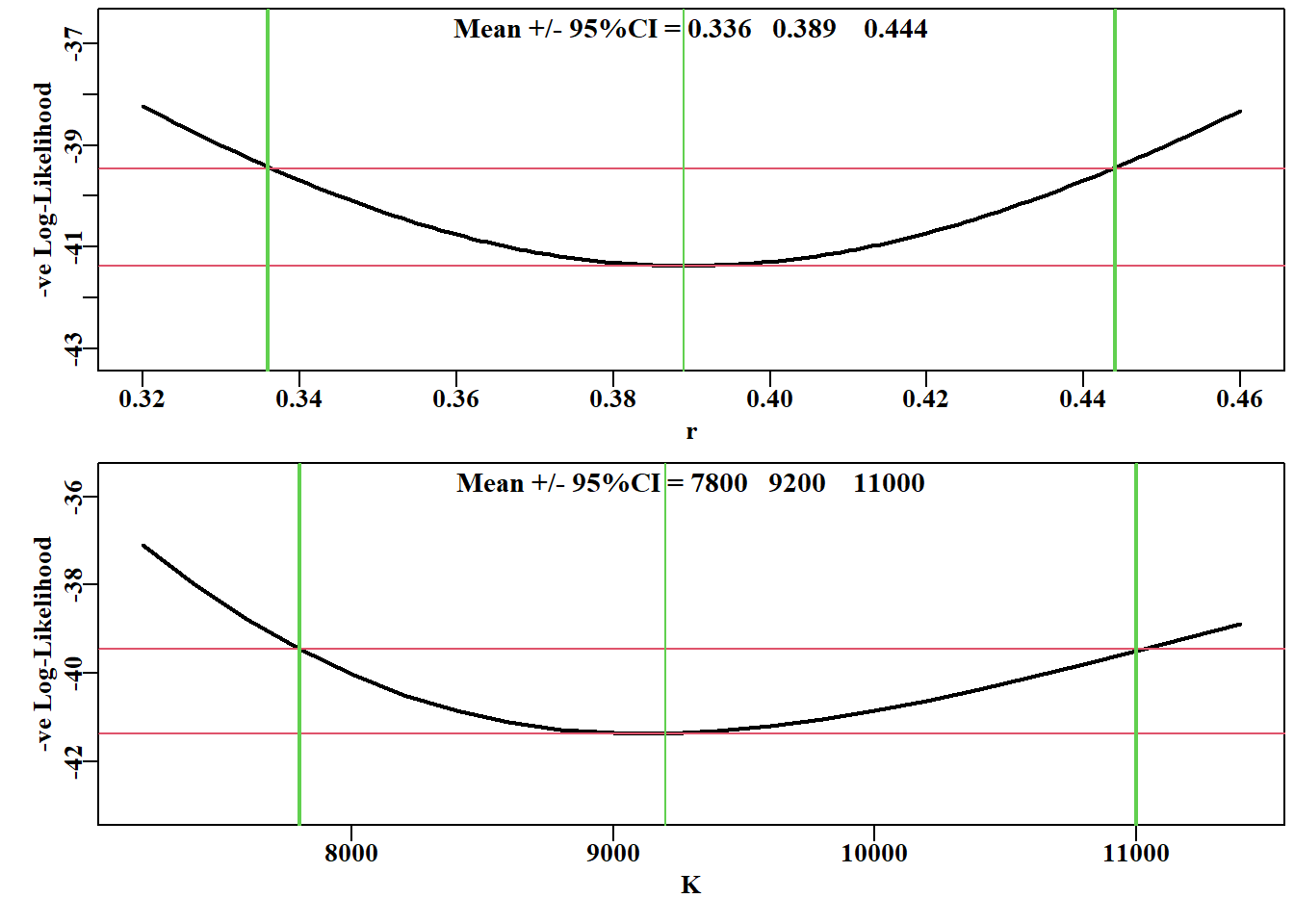

当我们测试一些模型拟合对初始条件的稳健性时,我们发现当拟合多个参数时,可以从略微不同的参数值中获得基本相同的数值拟合(达到给定的精度)。虽然这些值往往相差不大,但这一观察结果仍然证实,当使用数值方法估计一组参数时,特定参数值并不是唯一重要的结果。我们还需要知道这些估计的精确程度,我们需要知道与它们的估计相关的任何不确定性。有许多方法可以用来探索模型拟合中的不确定性。在这里,我们将使用 R 检查四个的实现:1)似然剖面,2)自举重采样,3) 渐近误差,以及 4)贝叶斯后验分布。

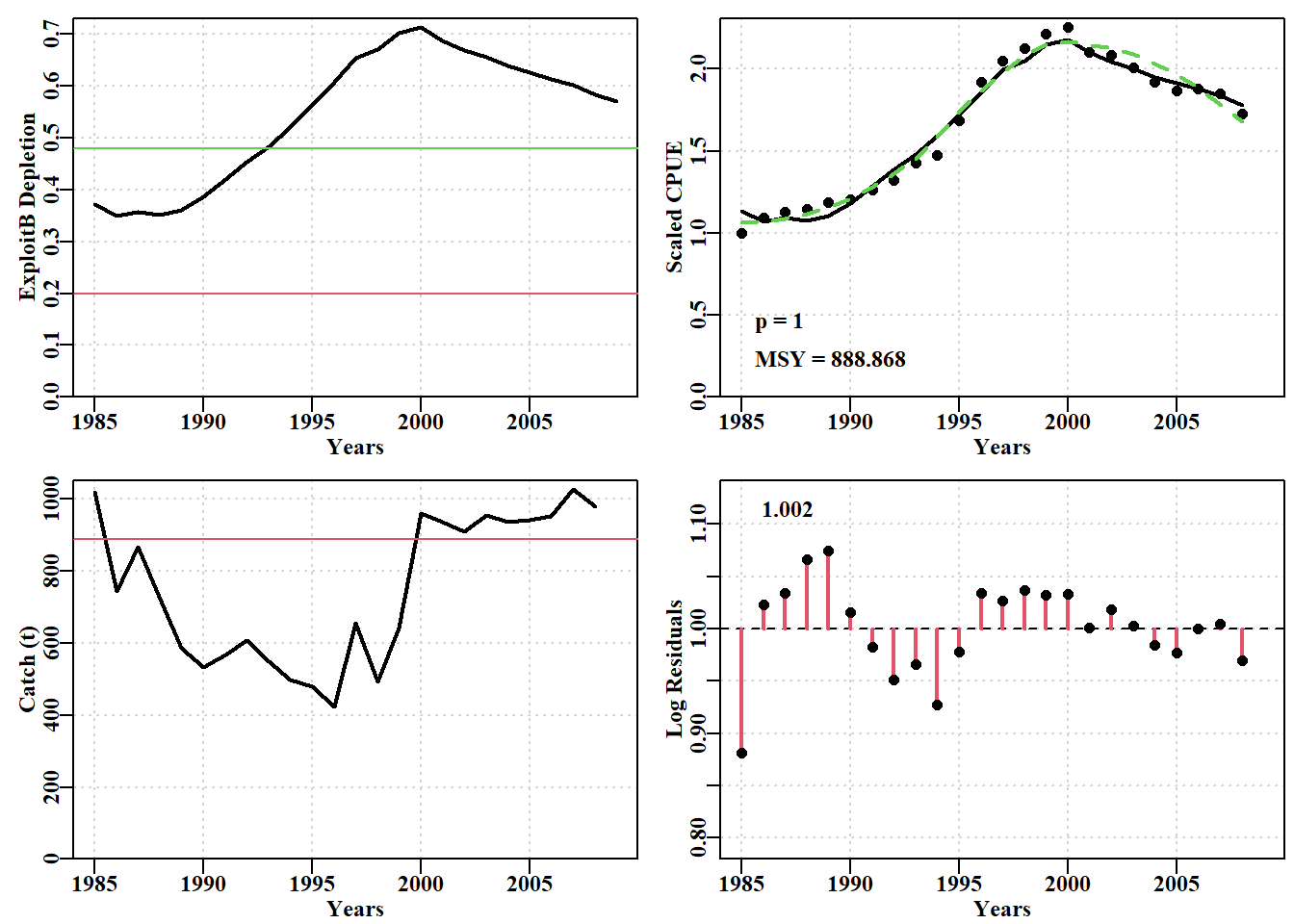

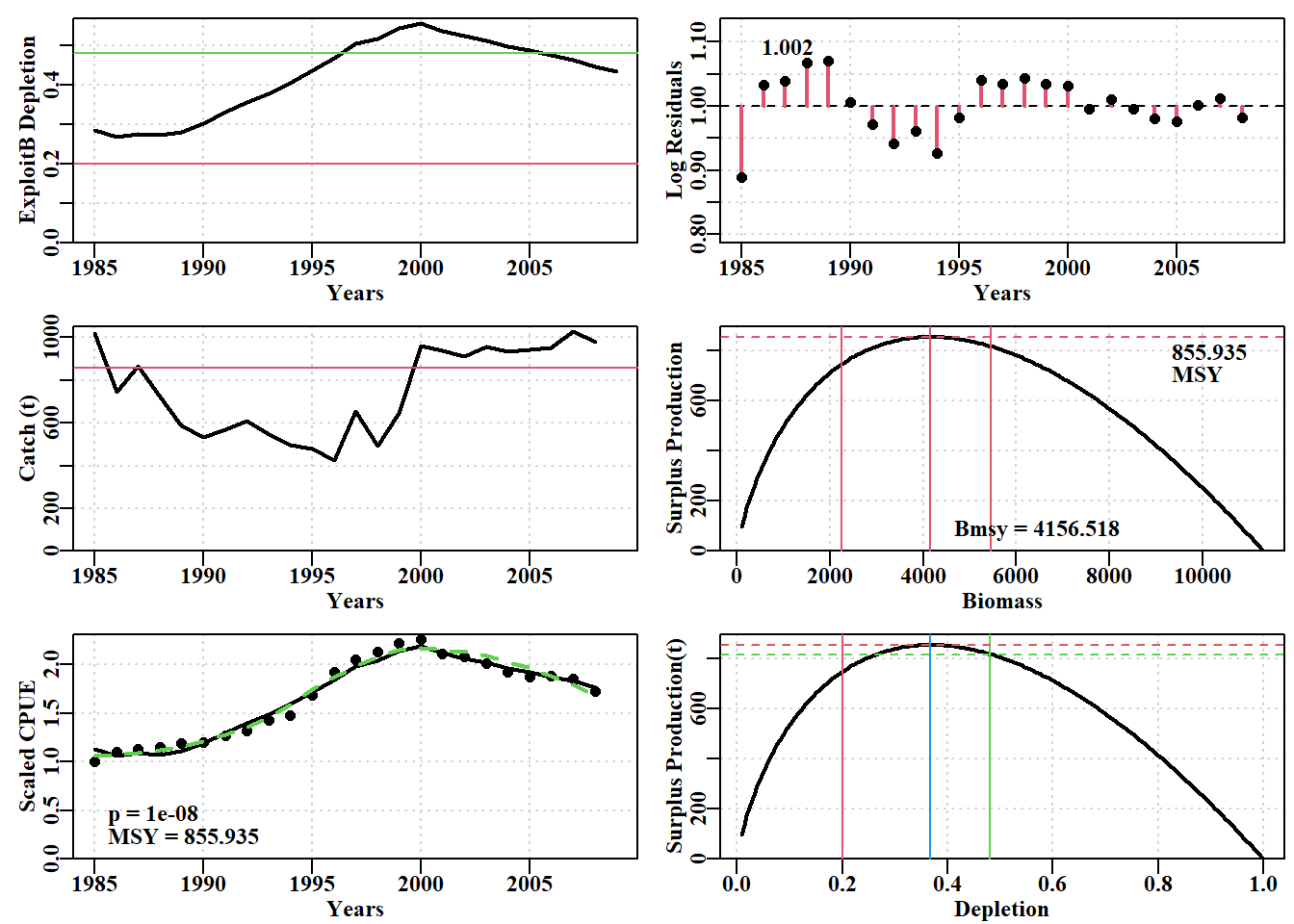

# Fig 7.9 Fit of optimum to the abdat data-setdata(abdat)fish<-as.matrix(abdat)colnames(fish)<-tolower(colnames(fish))# just in casepars<-log(c(r =0.4, K =9400, Binit =3400, sigma =0.05))ans<-fitSPM(pars, fish, schaefer =TRUE)# Schaeferanswer<-plotspmmod(ans$estimate, abdat, schaefer =TRUE, addrmse =TRUE)

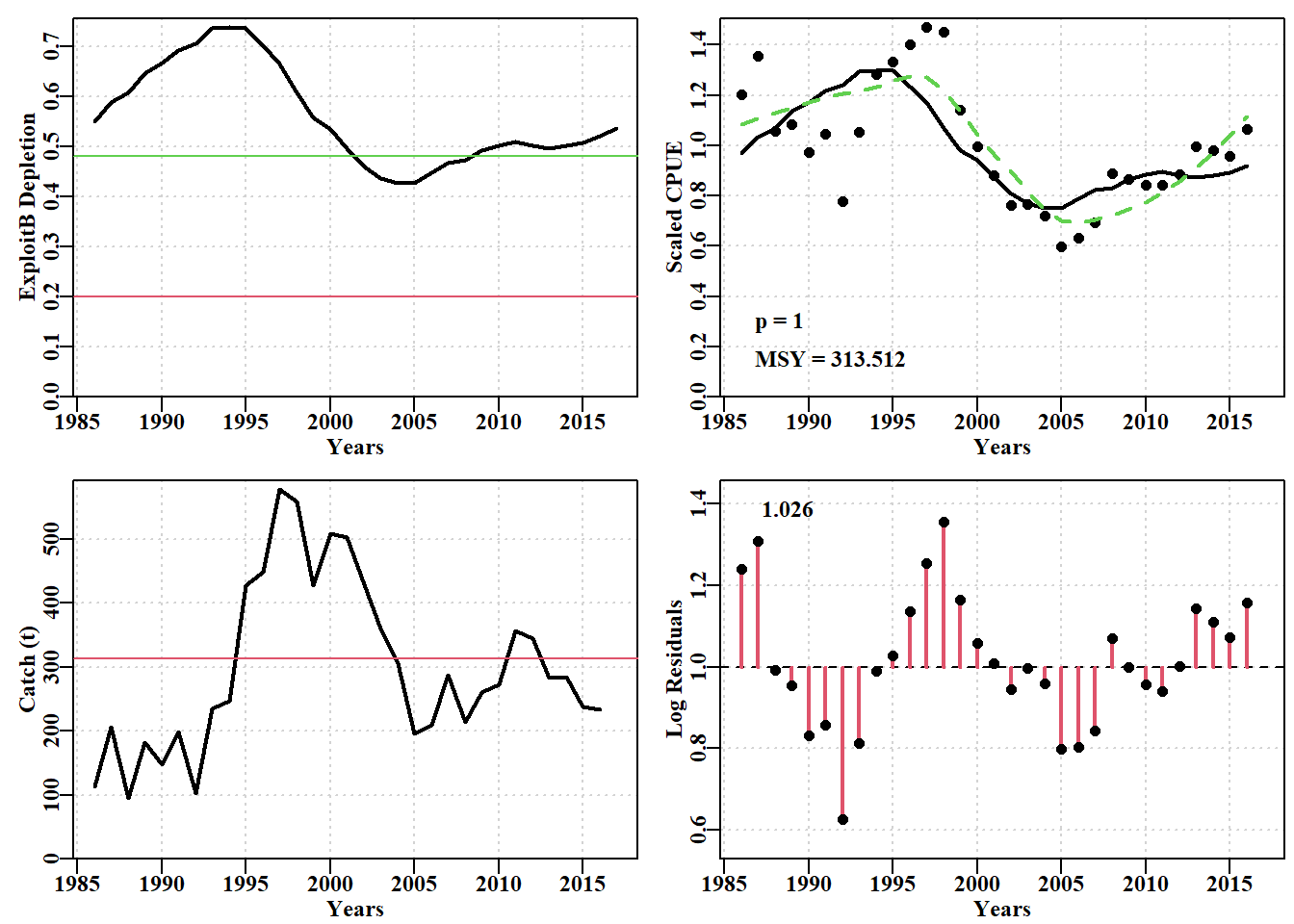

#find optimum Schaefer model fit to dataspm data-set Fig 7.11 data(dataspm)fish<-as.matrix(dataspm)colnames(fish)<-tolower(colnames(fish))pars<-log(c(r=0.25,K=5500,Binit=3000,sigma=0.25))ans<-fitSPM(pars,fish,schaefer=TRUE,maxiter=1000)#Schaefer answer<-plotspmmod(ans$estimate,fish,schaefer=TRUE,addrmse=TRUE)

#bootstrap the log-normal residuals from optimum model fit set.seed(210368)reps<-1000# can take 10 sec on a large Desktop. Be patient #startime <- Sys.time() # schaefer=TRUE is the default boots<-spmboot(ans$estimate,fishery=fish,iter=reps)#print(Sys.time() - startime) # how long did it take? str(boots,max.level=1)

List of 2

$ dynam : num [1:1000, 1:31, 1:5] 2846 3555 2459 3020 1865 ...

..- attr(*, "dimnames")=List of 3

$ bootpar: num [1:1000, 1:8] 0.242 0.236 0.192 0.23 0.361 ...

..- attr(*, "dimnames")=List of 2

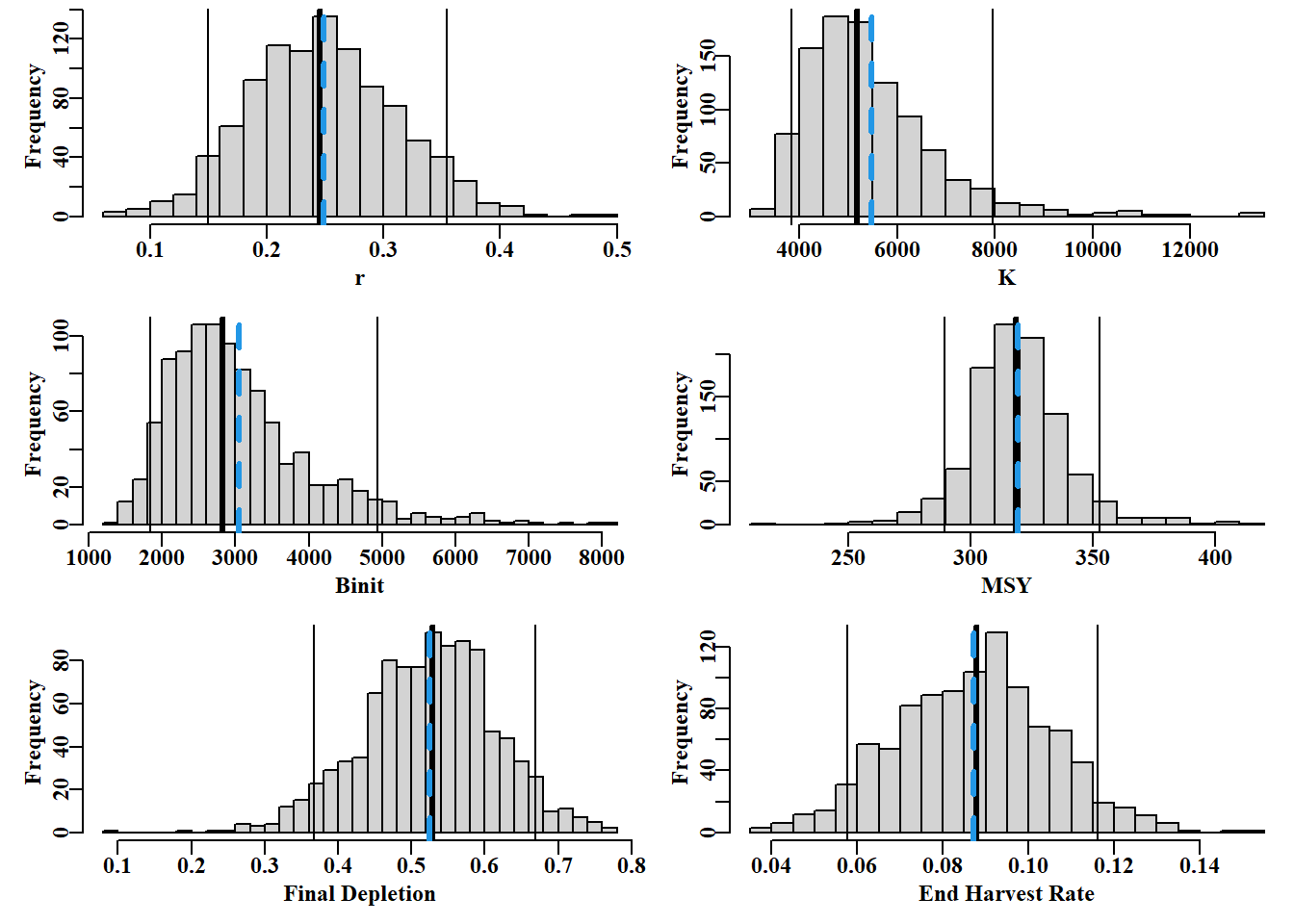

#boostrap CI. Note use of uphist to expand scale Fig 7.12 {colf<-c(1,1,1,4); lwdf<-c(1,3,1,3); ltyf<-c(1,1,1,2)colsf<-c(2,3,4,6)parset(plots=c(3,2))hist(bootpar[,"r"],breaks=25,main="",xlab="r")abline(v=c(bootCI["r",colsf]),col=colf,lwd=lwdf,lty=ltyf)uphist(bootpar[,"K"],maxval=14000,breaks=25,main="",xlab="K")abline(v=c(bootCI["K",colsf]),col=colf,lwd=lwdf,lty=ltyf)hist(bootpar[,"Binit"],breaks=25,main="",xlab="Binit")abline(v=c(bootCI["Binit",colsf]),col=colf,lwd=lwdf,lty=ltyf)uphist(bootpar[,"MSY"],breaks=25,main="",xlab="MSY",maxval=450)abline(v=c(bootCI["MSY",colsf]),col=colf,lwd=lwdf,lty=ltyf)hist(bootpar[,"Depl"],breaks=25,main="",xlab="Final Depletion")abline(v=c(bootCI["Depl",colsf]),col=colf,lwd=lwdf,lty=ltyf)hist(bootpar[,"Harv"],breaks=25,main="",xlab="End Harvest Rate")abline(v=c(bootCI["Harv",colsf]),col=colf,lwd=lwdf,lty=ltyf)}

图 7.12: The 1000 bootstrap replicates from the optimum spm fit to the dataspm data-set. The vertical lines, in each case, are the median and 90th percentile confidence intervals and the dashed vertical blue lines are the mean values. The function uphist() is used to expand the x-axis in K, Binit, and MSY.

存储在 boots$dynam 中的拟合轨迹也可以直观地指示分析的不确定性。

代码

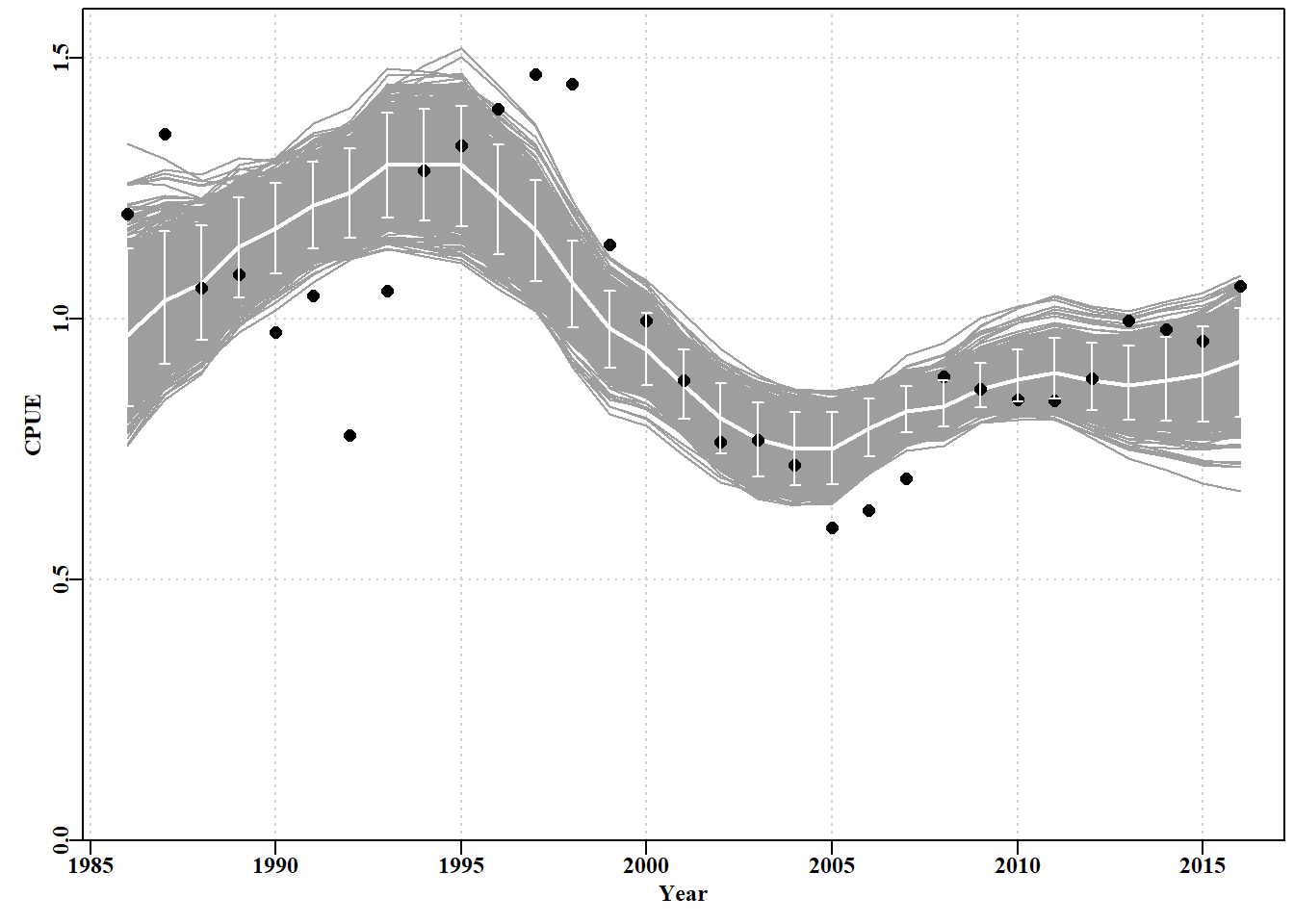

#Fig7.13 1000 bootstrap trajectories for dataspm model fit dynam<-boots$dynamyears<-fish[,"year"]nyrs<-length(years)parset()ymax<-getmax(c(dynam[,,"predCE"],fish[,"cpue"]))plot(fish[,"year"],fish[,"cpue"],type="n",ylim=c(0,ymax), xlab="Year",ylab="CPUE",yaxs="i",panel.first =grid())for(iin1:reps)lines(years,dynam[i,,"predCE"],lwd=1,col=8)lines(years,answer$Dynamics$outmat[1:nyrs,"predCE"],lwd=2,col=0)points(years,fish[,"cpue"],cex=1.2,pch=16,col=1)percs<-apply(dynam[,,"predCE"],2,quants)arrows(x0=years,y0=percs["5%",],y1=percs["95%",],length=0.03, angle=90,code=3,col=0)

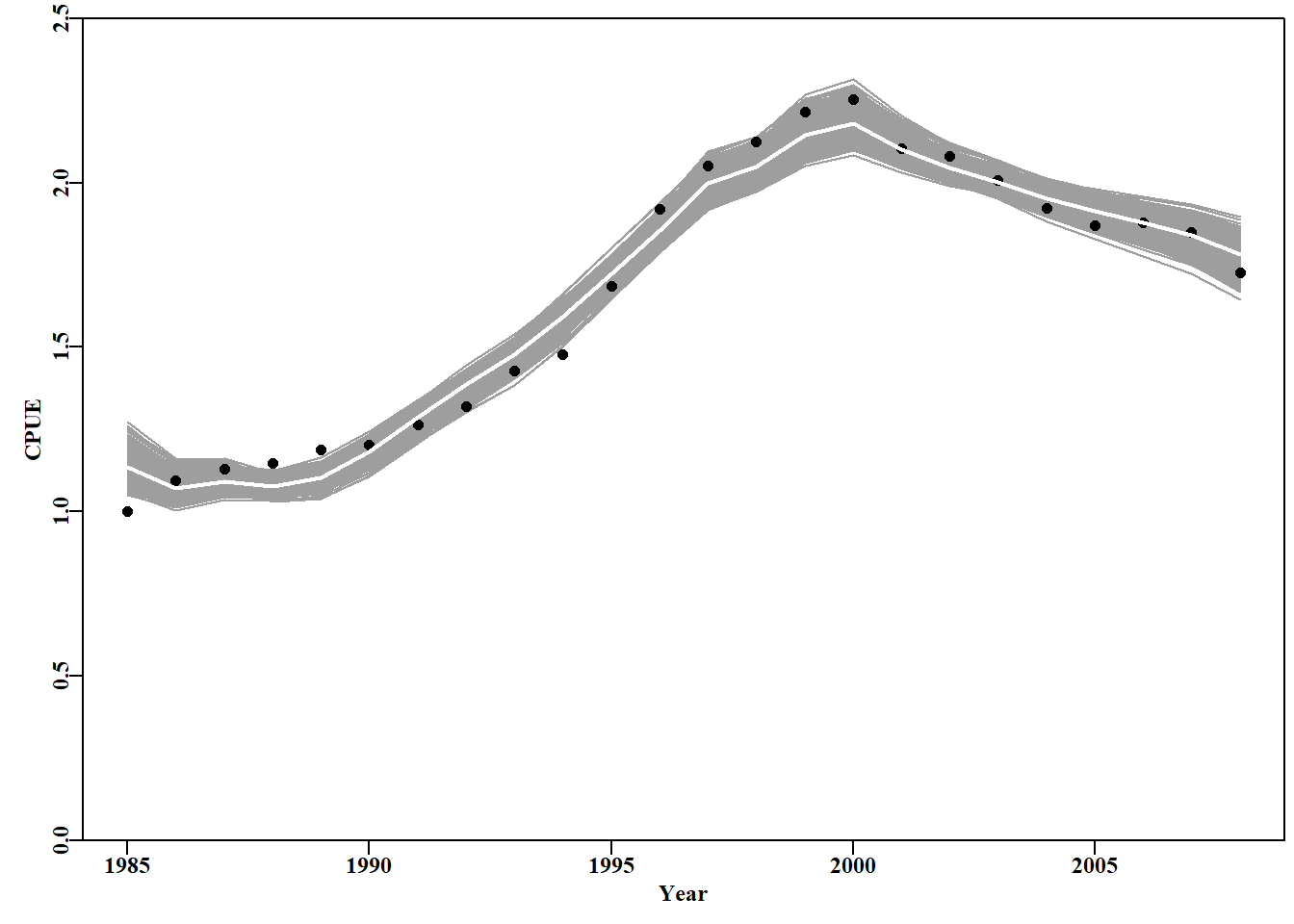

图 7.13: A plot of the original observed CPUE (black dots), the optimum predicted CPUE (solid line), the 1000 bootstrap predicted CPUE (the grey lines), and the 90th percentile confidence intervals around those predicted values (the vertical bars).

值得一做的是重复上述分析,但将 schaefer = TRUE 处改为 FALSE ,以便用 Fox 剩余产量模型来拟合模型。这样就可以比较两个模型的不确定性。

代码

#Fit the Fox model to dataspm; note different parameters pars<-log(c(r=0.15,K=6500,Binit=3000,sigma=0.20))ansF<-fitSPM(pars,fish,schaefer=FALSE,maxiter=1000)#Fox version bootsF<-spmboot(ansF$estimate,fishery=fish,iter=reps,schaefer=FALSE)dynamF<-bootsF$dynam

代码

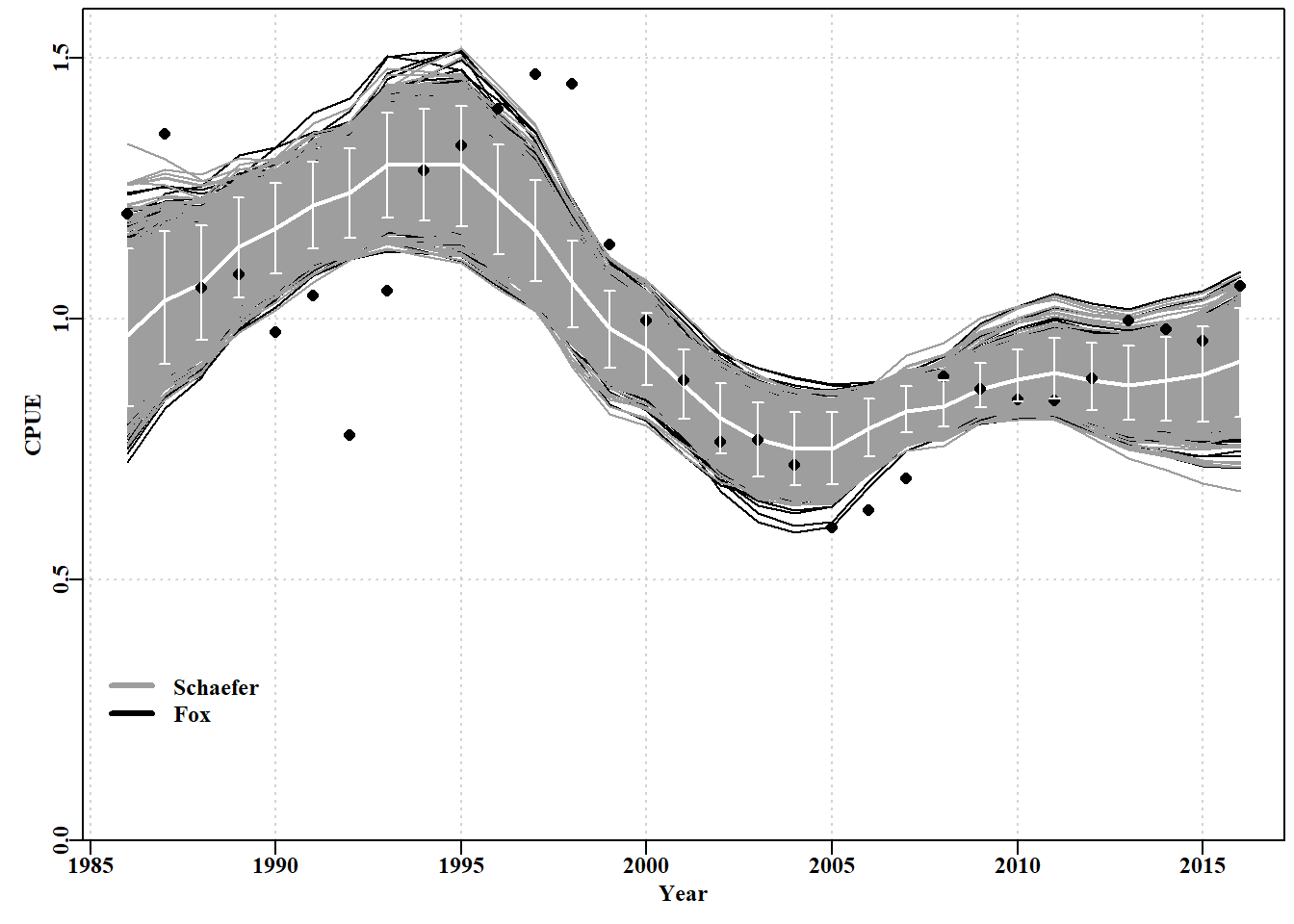

# bootstrap trajectories from both model fits Fig 7.14 parset()ymax<-getmax(c(dynam[,,"predCE"],fish[,"cpue"]))plot(fish[,"year"],fish[,"cpue"],type="n",ylim=c(0,ymax), xlab="Year",ylab="CPUE",yaxs="i",panel.first =grid())for(iin1:reps)lines(years,dynamF[i,,"predCE"],lwd=1,col=1,lty=1)for(iin1:reps)lines(years,dynam[i,,"predCE"],lwd=1,col=8)lines(years,answer$Dynamics$outmat[1:nyrs,"predCE"],lwd=2,col=0)points(years,fish[,"cpue"],cex=1.1,pch=16,col=1)percs<-apply(dynam[,,"predCE"],2,quants)arrows(x0=years,y0=percs["5%",],y1=percs["95%",],length=0.03, angle=90,code=3,col=0)legend(1985,0.35,c("Schaefer","Fox"),col=c(8,1),bty="n",lwd=3)

图 7.14: A plot of the original observed CPUE (dots), the optimum predicted CPUE (solid white line) with the 90th percentile confidence intervals (the white bars). The black lines are the Fox model bootstrap replicates while the grey lines over the black are those from the Schaefer model.

可以说,Fox 模型在捕捉这些数据的变异性方面更成功,因为黑线的扩散范围略大于灰色线(图 7.14)。或者,可以说 Fox 模型不太确定。总体而言,Schaefer 和 Fox 模型的输出之间没有太大差异,甚至像他们预测的那样 \(MSY\) 值非常相似(313.512 吨与 311.661 吨)。然而,最终,Fox 模型中密度依赖性的非线性似乎赋予了它更大的灵活性,因此它能够比更严格的 Schaefer 模型更好地捕获原始数据的变异性(因此它的 -ve 对数似然性更小,参见 outfit(ansF))。但这两个模型都无法捕获残差中表现出的循环特性,意味着建模动力学中未包含某些过程,即模型错误规范。这两种模型都不完全充分,尽管它们都可以提供足够的近似动态,可以用来产生管理建议(关于周期过程随时间保持不变的警告,等等)。

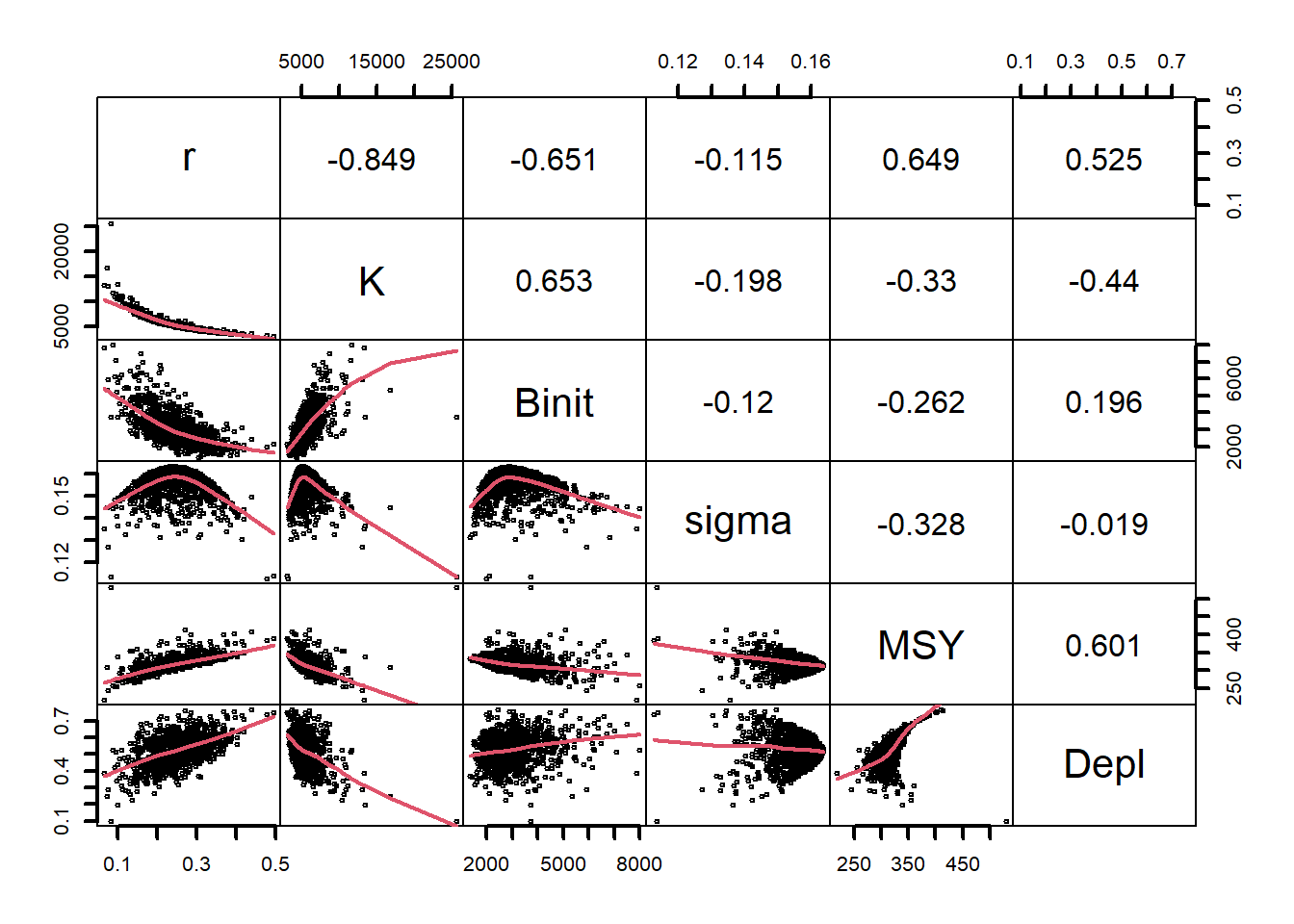

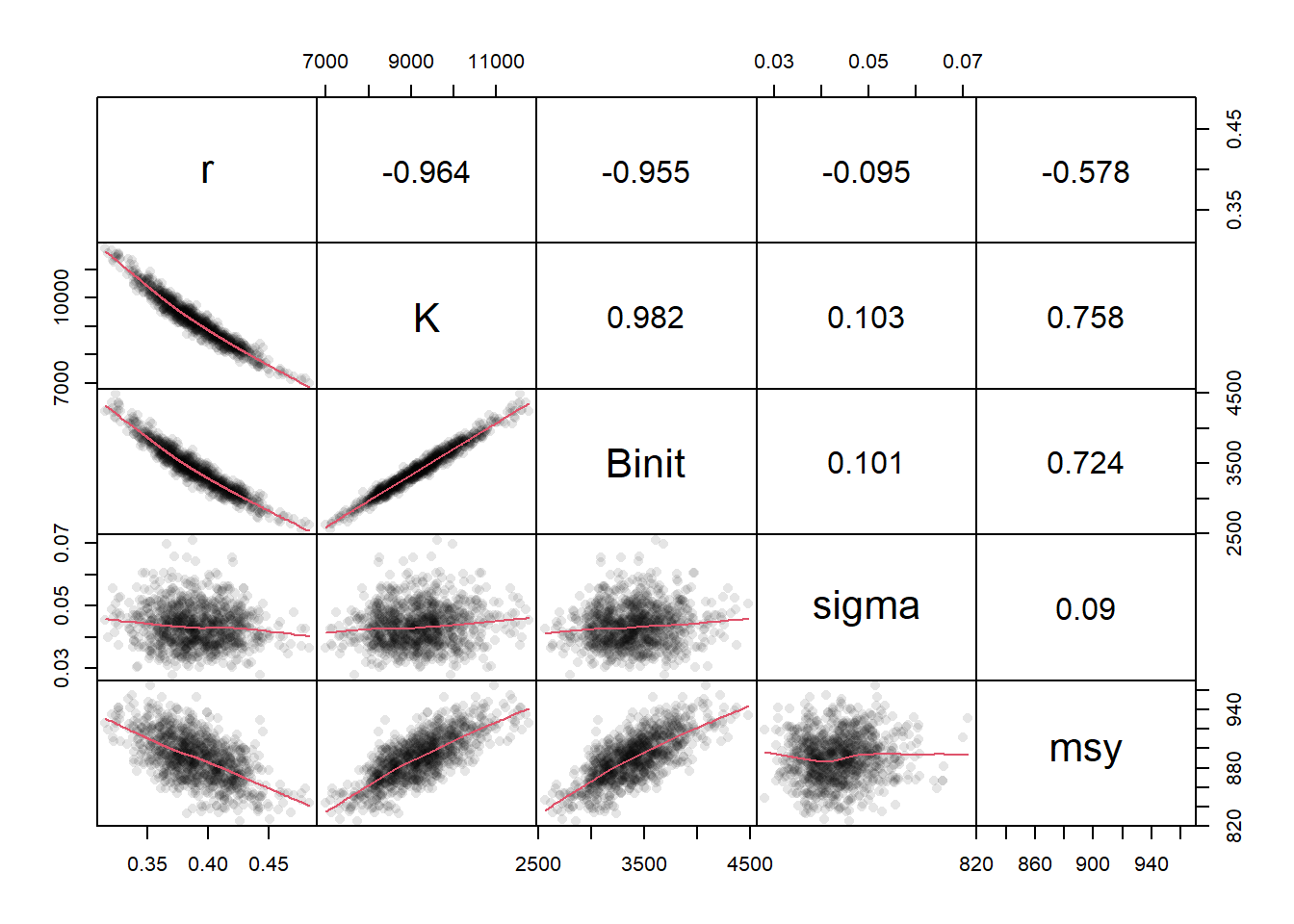

# plot variables against each other, use MQMF panel.cor Fig 7.15 pairs(boots$bootpar[,c(1:4,6,7)],lower.panel=panel.smooth, upper.panel=panel.cor,gap=0,lwd=2,cex=0.5)

图 7.15: 模型参数与 Schaefer 模型( Fox 模型使用 bootsF$bootpar)的一些输出之间的关系。下方面板在数据中具有一条红色的平滑线,用于说明任何趋势,而上方面板具有线性相关系数。少数极值会扭曲绘图。The relationships between the model parameters and some outputs for the Schaefer model (use bootsF$bootpar for the Fox model ). The lower panels have a red smoother line through the data illustrating any trends, while the upper panels have the linear correlation coefficient. The few extreme values distort the plots.

#Start the SPM analysis using asymptotic errors. data(dataspm)# Note the use of hess=TRUE in call to fitSPM fish<-as.matrix(dataspm)# using as.matrix for more speed colnames(fish)<-tolower(colnames(fish))# just in casepars<-log(c(r=0.25,K=5200,Binit=2900,sigma=0.20))ans<-fitSPM(pars,fish,schaefer=TRUE,maxiter=1000,hess=TRUE)

#calculate the var-covar matrix and the st errors vcov<-solve(ans$hessian)# calculate variance-covariance matrix label<-c("r","K", "Binit","sigma")colnames(vcov)<-label; rownames(vcov)<-labeloutvcov<-rbind(vcov,sqrt(diag(vcov)))rownames(outvcov)<-c(label,"StErr")

表 7.6: The variance-covariance (vcov) matrix is the inverse of the Hessian and the parameter standard errors are the square-root of the diagonal of the vcov matrix.

#generate 1000 parameter vectors from multi-variate normal library(mvtnorm)# use RStudio, or install.packages("mvtnorm") N<-1000# number of parameter vectors, use vcov from above mvn<-length(fish[,"year"])#matrix to store cpue trajectories mvncpue<-matrix(0,nrow=N,ncol=mvn,dimnames=list(1:N,fish[,"year"]))columns<-c("r","K","Binit","sigma")optpar<-ans$estimate# Fill matrix with mvn parameter vectors mvnpar<-matrix(exp(rmvnorm(N,mean=optpar,sigma=vcov)),nrow=N, ncol=4,dimnames=list(1:N,columns))msy<-mvnpar[,"r"]*mvnpar[,"K"]/4nyr<-length(fish[,"year"])depletion<-numeric(N)#now calculate N cpue series in linear space for(iin1:N){# calculate dynamics for each parameter set dynamA<-spm(log(mvnpar[i,1:4]),fish)mvncpue[i,]<-dynamA$outmat[1:nyr,"predCE"]depletion[i]<-dynamA$outmat["2016","Depletion"]}mvnpar<-cbind(mvnpar,msy,depletion)# try head(mvnpar,10)

#data and trajectories from 1000 MVN parameter vectors Fig 7.16 plot1(fish[,"year"],fish[,"cpue"],type="p",xlab="Year",ylab="CPUE", maxy=2.0)for(iin1:N)lines(fish[,"year"],mvncpue[i,],col="grey",lwd=1)points(fish[,"year"],fish[,"cpue"],pch=1,cex=1.3,col=1,lwd=2)# data lines(fish[,"year"],exp(simpspm(optpar,fish)),lwd=2,col=1)# pred percs<-apply(mvncpue,2,quants)# obtain the quantiles arrows(x0=fish[,"year"],y0=percs["5%",],y1=percs["95%",],length=0.03, angle=90,code=3,col=1)#add 90% quantiles msy<-mvnpar[,"r"]*mvnpar[,"K"]/4# 1000 MSY estimates text(2010,1.75,paste0("MSY ",round(mean(msy),3)),cex=1.25,font=7)

图 7.16: 从最优参数及其相关方差-协方差矩阵定义的多变量正态分布中采样的随机参数向量得出的 1000 条 cpue 预测轨迹。The 1000 predicted cpue trajectories derived from random parameter vectors sampled from the multi-variate normal distribution defined by the optimum parameters and their related variance-covariance matrix.

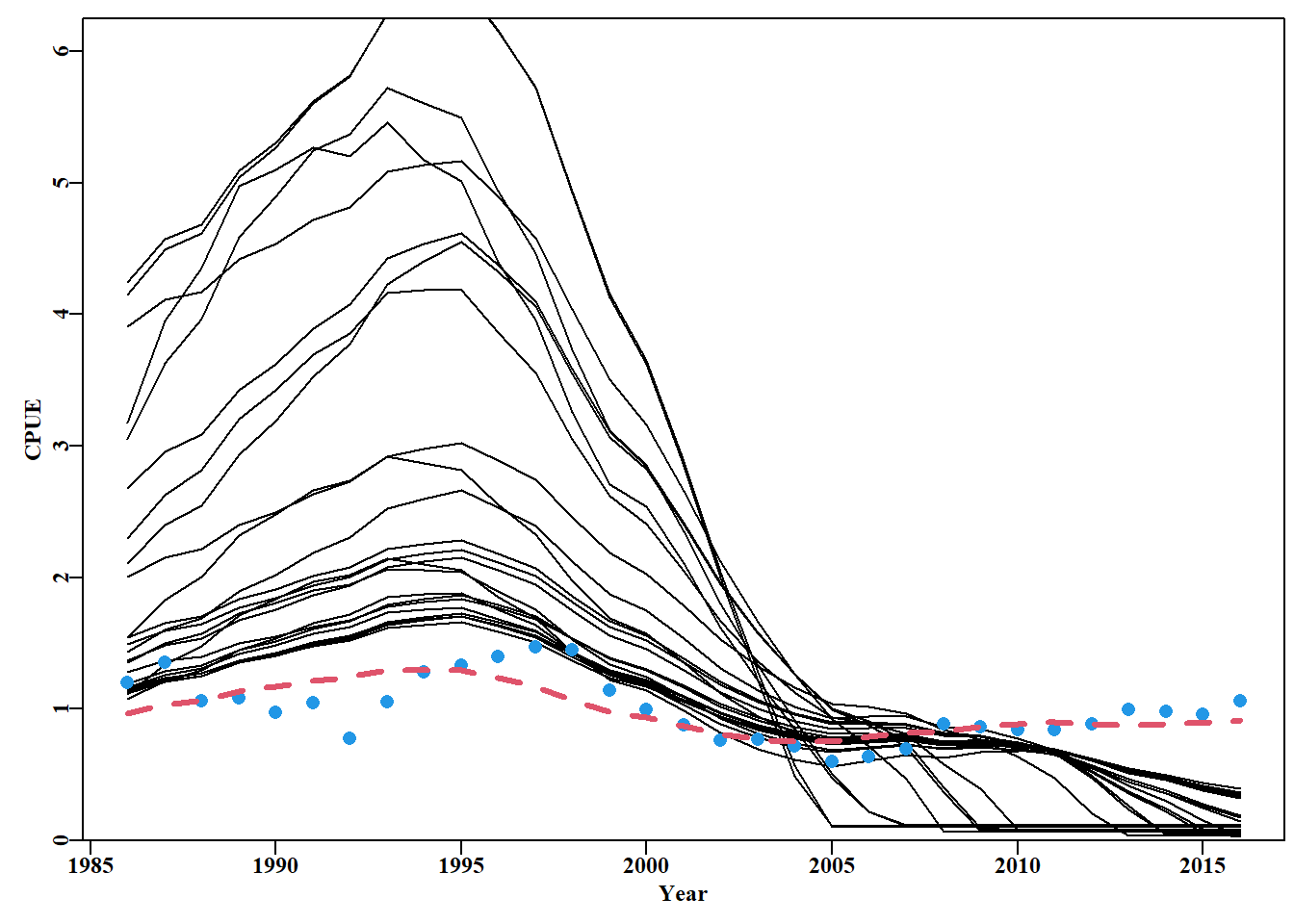

图 7.17: 预测 2016 年 cpue < 0.4 的 34 个渐近误差 cpue 轨迹。圆点为原始数据,虚线为最佳拟合模型。The 34 asymptotic error cpue trajectories that were predicted to have a cpue < 0.4 in 2016. The dots are the original data and the dashed line the optimum model fit.

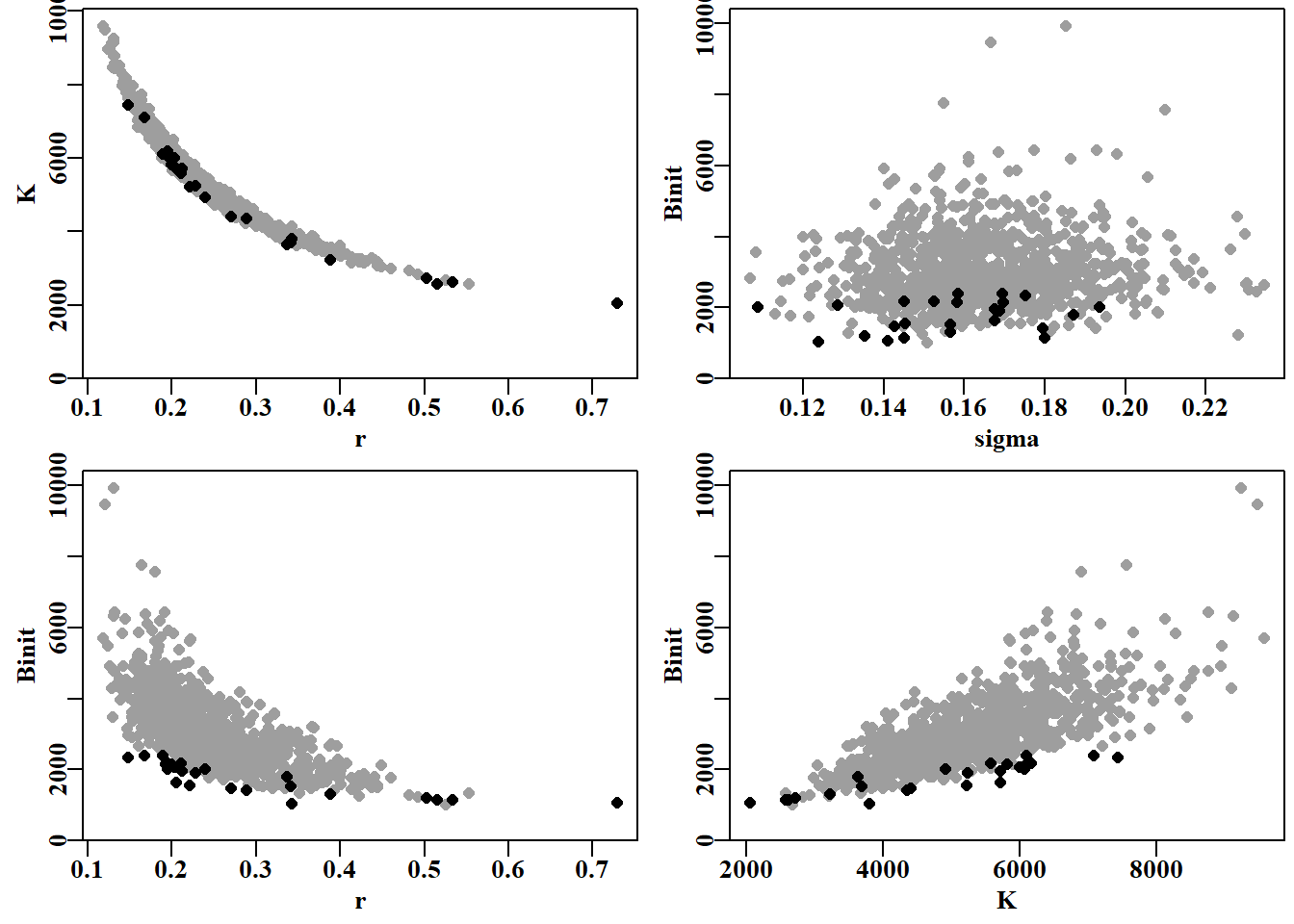

#Use adhoc function to plot errant parameters Fig 7.18 parset(plots=c(2,2),cex=0.85)outplot<-function(var1,var2,pickdev){plot1(mvnpar[,var1],mvnpar[,var2],type="p",pch=16,cex=1.0, defpar=FALSE,xlab=var1,ylab=var2,col=8)points(mvnpar[pickdev,var1],mvnpar[pickdev,var2],pch=16,cex=1.0)}outplot("r","K",pickd)# assumes mvnpar in working environment outplot("sigma","Binit",pickd)outplot("r","Binit",pickd)outplot("K","Binit",pickd)

图 7.18: 渐近误差样本中参数值的分布,黑色部分为预测最终 cpue < 0.4 的参数值。看来,Binit 的低值是造成难以置信轨迹的主要原因。The spread of parameter values from the asymptotic error samples with the values that predicted final cpue < 0.4 highlighted in black. It appears that low values of Binit are mostly behind the implausible trajectories.

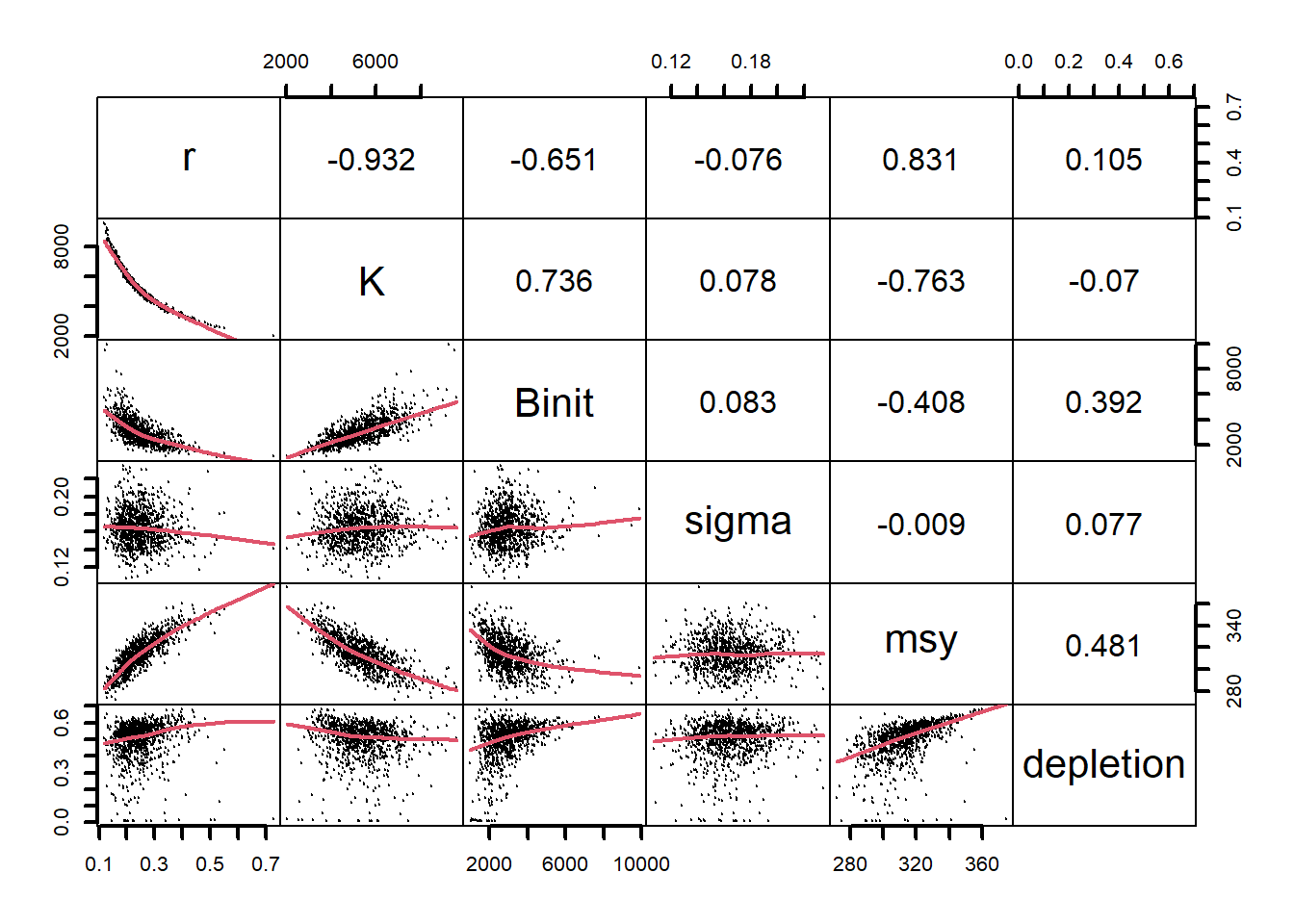

图 7.19: 使用多变量正态分布生成参数组合时 Schaefer 模型参数之间的关系。r - K 之间的关系比自举样本紧密得多,而 sigma 与其他参数之间几乎没有关系。损耗图显示一些轨迹已经消失。The relationships between the model parameters for the Schaefer model when using the multi-variate normal distribution to generate the parameter combinations. The relationship between r - K is much tighter than in the bootstrap samples and there is almost no relationship between sigma and the other parameters. The depletion plots indicate some trajectories go extinct.

# Get the ranges of parameters from bootstrap and asymptotic bt<-apply(bootpar,2,range)[,c(1:4,6,7)]ay<-apply(mvnpar,2,range)out<-rbind(bt,ay)rownames(out)<-c("MinBoot","MaxBoot","MinAsym","MaxAsym")

表 7.7: 自举取样与渐近误差取样的参数值范围对比。The range of parameter values from the bootstrap sampling compared with those from the Asymptotic Error sampling.

#repeat asymptotice errors using abdat data-set Figure 7.20 data(abdat)fish<-as.matrix(abdat)pars<-log(c(r=0.4,K=9400,Binit=3400,sigma=0.05))ansA<-fitSPM(pars,fish,schaefer=TRUE,maxiter=1000,hess=TRUE)vcovA<-solve(ansA$hessian)# calculate var-covar matrix mvn<-length(fish[,"year"])N<-1000# replicates mvncpueA<-matrix(0,nrow=N,ncol=mvn,dimnames=list(1:N,fish[,"year"]))columns<-c("r","K","Binit","sigma")optparA<-ansA$estimate# Fill matrix of parameter vectors mvnparA<-matrix(exp(rmvnorm(N,mean=optparA,sigma=vcovA)), nrow=N,ncol=4,dimnames=list(1:N,columns))msy<-mvnparA[,"r"]*mvnparA[,"K"]/4for(iin1:N)mvncpueA[i,]<-exp(simpspm(log(mvnparA[i,]),fish))mvnparA<-cbind(mvnparA,msy)plot1(fish[,"year"],fish[,"cpue"],type="p",xlab="Year",ylab="CPUE", maxy=2.5)for(iin1:N)lines(fish[,"year"],mvncpueA[i,],col=8,lwd=1)points(fish[,"year"],fish[,"cpue"],pch=16,cex=1.0)#orig data lines(fish[,"year"],exp(simpspm(optparA,fish)),lwd=2,col=0)

图 7.20: 利用渐近误差为 abdat 数据集生成可信的参数集及其隐含的 cpue 轨迹。最佳拟合模型以白线表示。The use of asymptotic errors to generate plausible parameter sets and their implied cpue trajectories for the abdat data-set. The optimum model fit is shown as a white line.

图 7.21: 将 Schaefer 模型拟合到 abdat 数据并使用多变量正态分布生成后续参数组合时的模型参数关系。这与 “不确定性”一章中的自举法非常相似。Model parameter relationships when fitting the Schaefer model to the abdat data and using the multi-variate normal distribution to generate subsequent parameter combinations. These are very similar to the bootstrap equivalent in the On Uncertainty chapter.

#Fit the Fox Model to the abdat data Figure 7.22 data(abdat); fish<-as.matrix(abdat)param<-log(c(r=0.3,K=11500,Binit=3300,sigma=0.05))foxmod<-nlm(f=negLL1,p=param,funk=simpspm,indat=fish, logobs=log(fish[,"cpue"]),iterlim=1000,schaefer=FALSE)optpar<-exp(foxmod$estimate)ans<-plotspmmod(inp=foxmod$estimate,indat=fish,schaefer=FALSE, addrmse=TRUE, plotprod=TRUE)

图 7.22: 使用 Fox 模型和对数正态误差拟合的 abdat 数据集最佳模型。绿色虚线是较平滑的曲线,红线是最佳预测模型拟合。请注意对数正态残差的模式,这表明该模型在该数据方面存在微小不足。The optimum model fit for the abdat data-set using the Fox model and log-normal errors. The green dashed line is a smoother curve while the red line is the optimum predicted model fit. Note the pattern in the log-normal residuals indicating that the model has small inadequacies with regard to this data.

#|echo: falselibrary(Rcpp)cppFunction('NumericVector simpspmC(NumericVector pars, NumericMatrix indat, LogicalVector schaefer) { int nyrs = indat.nrow(); NumericVector predce(nyrs); NumericVector biom(nyrs+1); double Bt, qval; double sumq = 0.0; double p = 0.00000001; if (schaefer(0) == TRUE) { p = 1.0; } NumericVector ep = exp(pars); biom[0] = ep[2]; for (int i = 0; i < nyrs; i++) { Bt = biom[i]; biom[(i+1)] = Bt + (ep[0]/p)*Bt*(1 - pow((Bt/ep[1]),p)) - indat(i,1); if (biom[(i+1)] < 40.0) biom[(i+1)] = 40.0; sumq += log(indat(i,2)/biom[i]); } qval = exp(sumq/nyrs); for (int i = 0; i < nyrs; i++) { predce[i] = log(biom[i] * qval); } return predce; }')

代码

# eval: false# Conduct an MCMC using simpspmC on the abdat Fox SPM # This means you will need to compile simpspmC from appendix set.seed(698381)#for repeatability, possibly only on Windows10 begin<-gettime()# to enable the time taken to be calculated inscale<-c(0.07,0.05,0.09,0.45)#note large value for sigma pars<-log(c(r=0.205,K=11300,Binit=3200,sigma=0.044))result<-do_MCMC(chains=1,burnin=50,N=2000,thinstep=512, inpar=pars,infunk=negLL,calcpred=simpspm, obsdat=log(fish[,"cpue"]),calcdat=fish, priorcalc=calcprior,scales=inscale,schaefer=FALSE)# alternatively, use simpspm, but that will take longer. cat("acceptance rate = ",result$arate," \n")

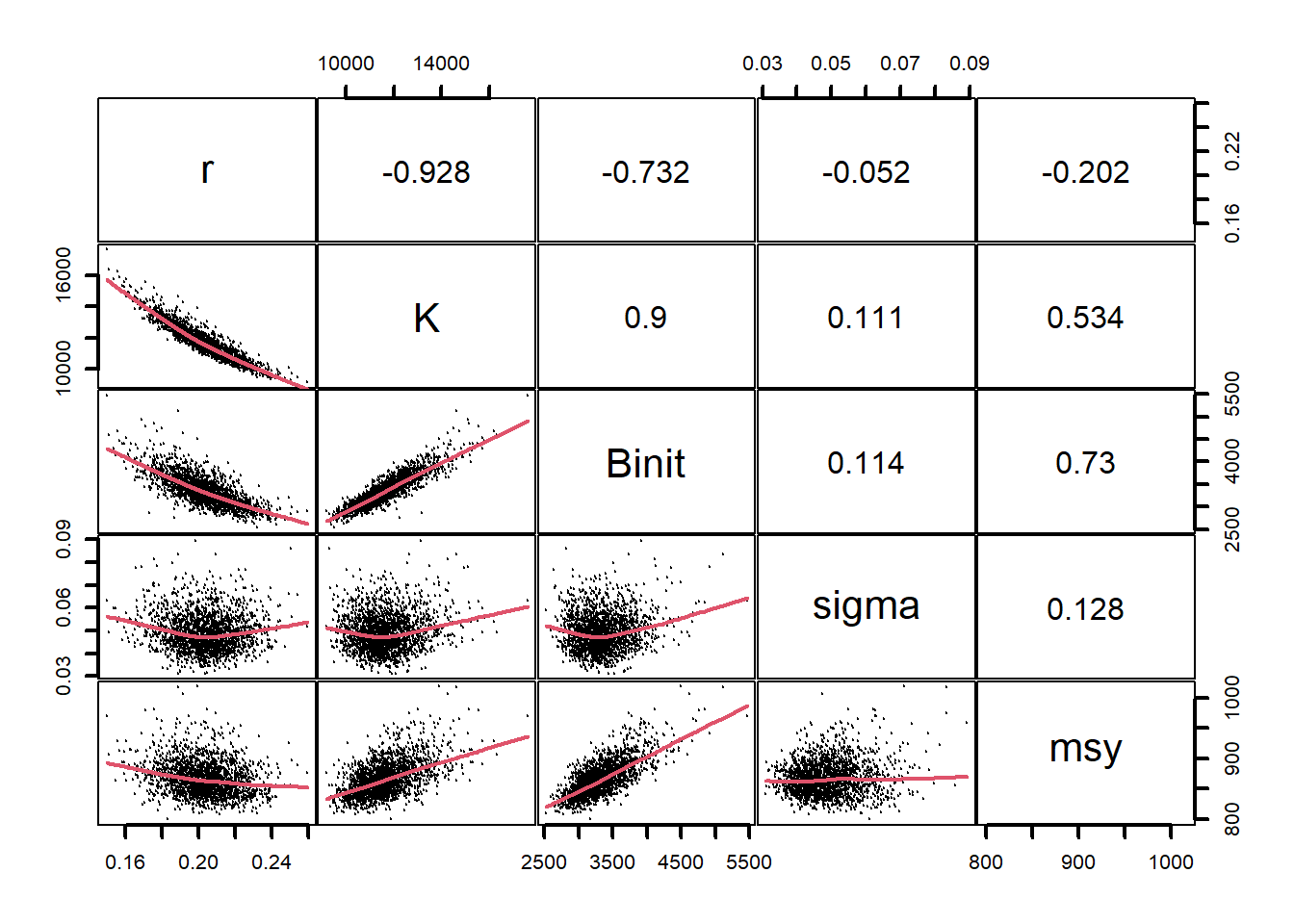

#pairwise comparison for MCMC of Fox model on abdat Fig 7.23 pairs(cbind(post1[,1:4],msy),upper.panel =panel.cor,lwd=2,cex=0.2, lower.panel=panel.smooth,col=1,gap=0.1)

图 7.23: MCMC 输出的成对散点图。实线是表示趋势的塬平滑线,上半部分的数字是成对散点图之间的相关系数。r、K 和 Binit 之间,以及 K、Binit 和 MSY 之间都有很强的相关性,而 sigma 与其他参数或 msy 与 r 之间的关系较小或没有关系。MCMC output as paired scattergrams. The solid lines are loess smoothers indicating trends and the numbers in the upper half are the correlation coefficients between the pairs. Strong correlations are indicated between r, K, and Binit, and between K, Binit, and MSY, with only minor or no relationships between sigma the other parameters or between msy and r.

代码

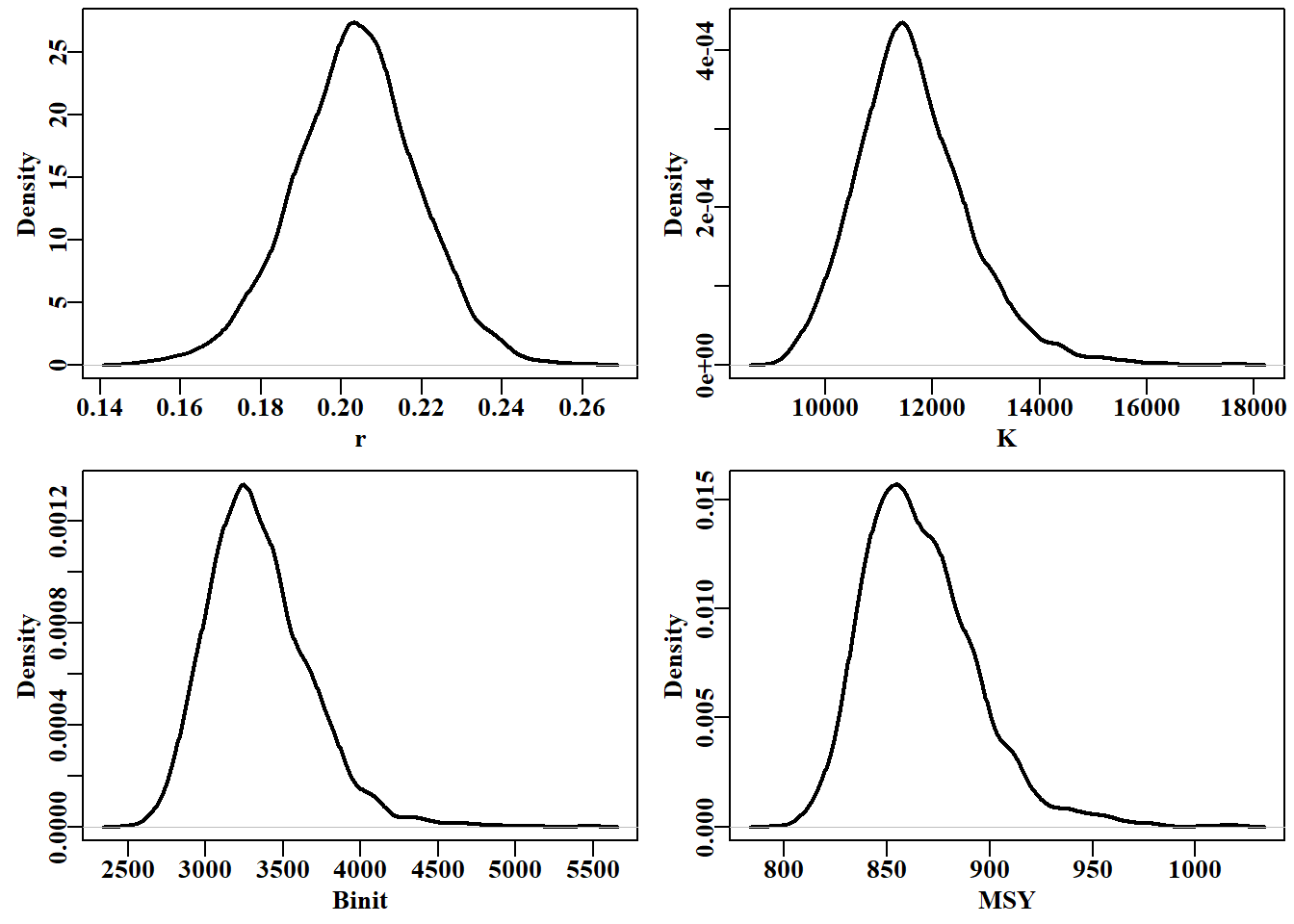

# marginal distributions of 3 parameters and msy Figure 7.24 parset(plots=c(2,2), cex=0.85)plot(density(post1[,"r"]),lwd=2,main="",xlab="r")#plot has a method plot(density(post1[,"K"]),lwd=2,main="",xlab="K")#for output from plot(density(post1[,"Binit"]),lwd=2,main="",xlab="Binit")# density plot(density(msy),lwd=2,main="",xlab="MSY")#try str(density(msy))

图 7.24: 将 Fox 模型应用于鳕鱼数据的 2000 次 MCMC 重复计算得出的三个参数的边际分布和隐含的 MSY。曲线的块状表明需要进行 2000 次以上的迭代。The marginal distributions for three parameters and the implied MSY from 2000 MCMC replicates for the Fox model applied to the abdat data. The lumpiness of the curves suggests more than 2000 iterations are needed.

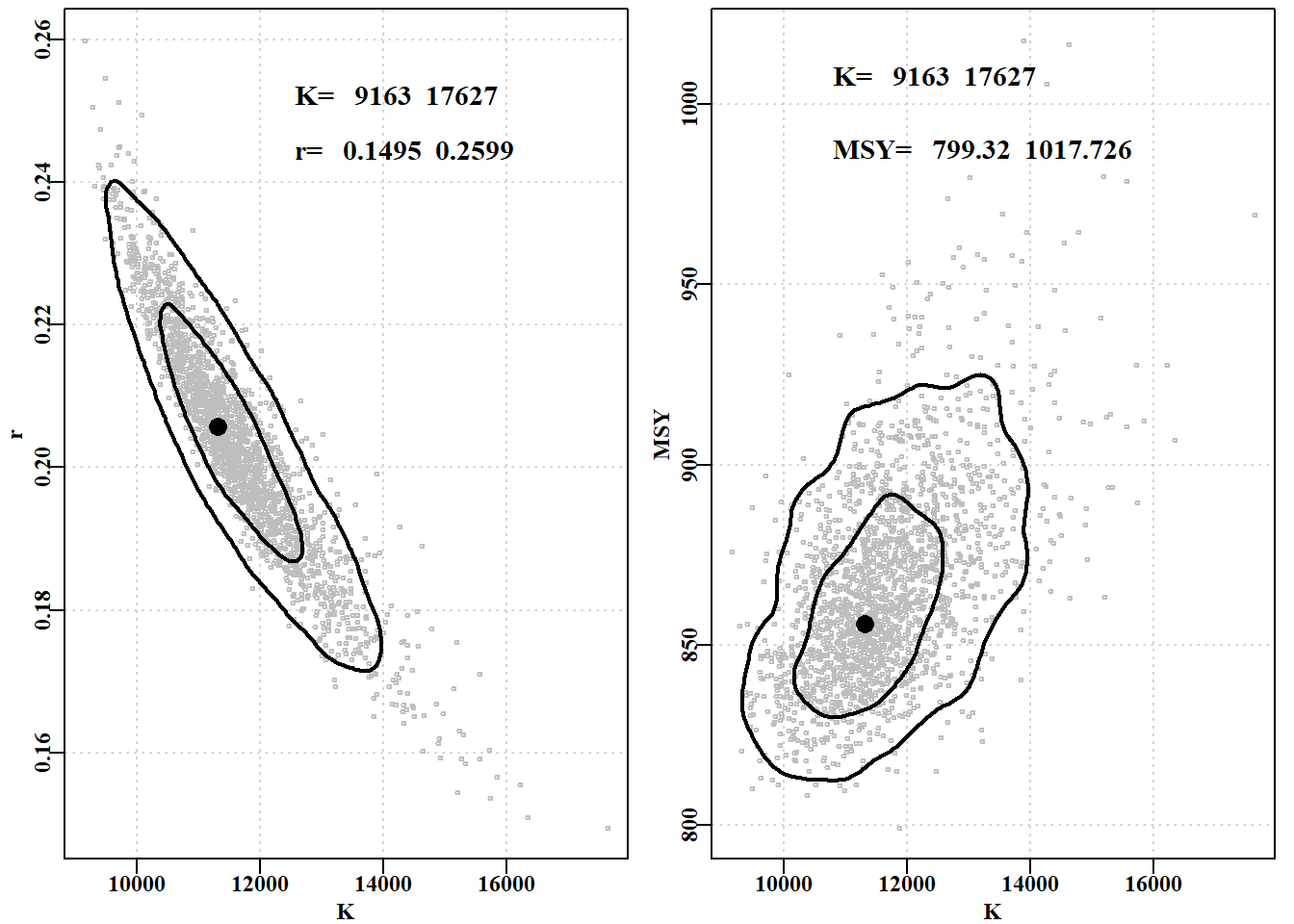

#MCMC r and K parameters, approx 50 + 90% contours. Fig7.25 puttxt<-function(xs,xvar,ys,yvar,lvar,lab="",sigd=0){text(xs*xvar[2],ys*yvar[2],makelabel(lab,lvar,sep=" ", sigdig=sigd),cex=1.2,font=7,pos=4)}# end of puttxt - a quick utility function kran<-range(post1[,"K"]); rran<-range(post1[,"r"])mran<-range(msy)#ranges used in the plots parset(plots=c(1,2),margin=c(0.35,0.35,0.05,0.1))#plot r vs K plot(post1[,"K"],post1[,"r"],type="p",cex=0.5,xlim=kran, ylim=rran,col="grey",xlab="K",ylab="r",panel.first=grid())points(optpar[2],optpar[1],pch=16,col=1,cex=1.75)# center addcontours(post1[,"K"],post1[,"r"],kran,rran, #if fails make contval=c(0.5,0.9),lwd=2,col=1)#contval smaller puttxt(0.7,kran,0.97,rran,kran,"K= ",sigd=0)puttxt(0.7,kran,0.94,rran,rran,"r= ",sigd=4)plot(post1[,"K"],msy,type="p",cex=0.5,xlim=kran, # K vs msy ylim=mran,col="grey",xlab="K",ylab="MSY",panel.first=grid())points(optpar[2],getMSY(optpar,p),pch=16,col=1,cex=1.75)#center addcontours(post1[,"K"],msy,kran,mran,contval=c(0.5,0.9),lwd=2,col=1)puttxt(0.6,kran,0.99,mran,kran,"K= ",sigd=0)puttxt(0.6,kran,0.97,mran,mran,"MSY= ",sigd=3)

图 7.25: MCMC 边际分布输出为 r 和 K 参数以及 K 和 MSY 值的散点图。灰点是成功的候选参数向量,等值线是近似的第 50 和第 90 分位数。文中给出了全部可接受的参数迹线范围。MCMC marginal distributions output as a scattergram of the r and K parameters, and the K and MSY values. The grey dots are from successful candidate parameter vectors, while the contours are approximate 50th and 90th percentiles. The text give the full range of the accepted parameter traces.

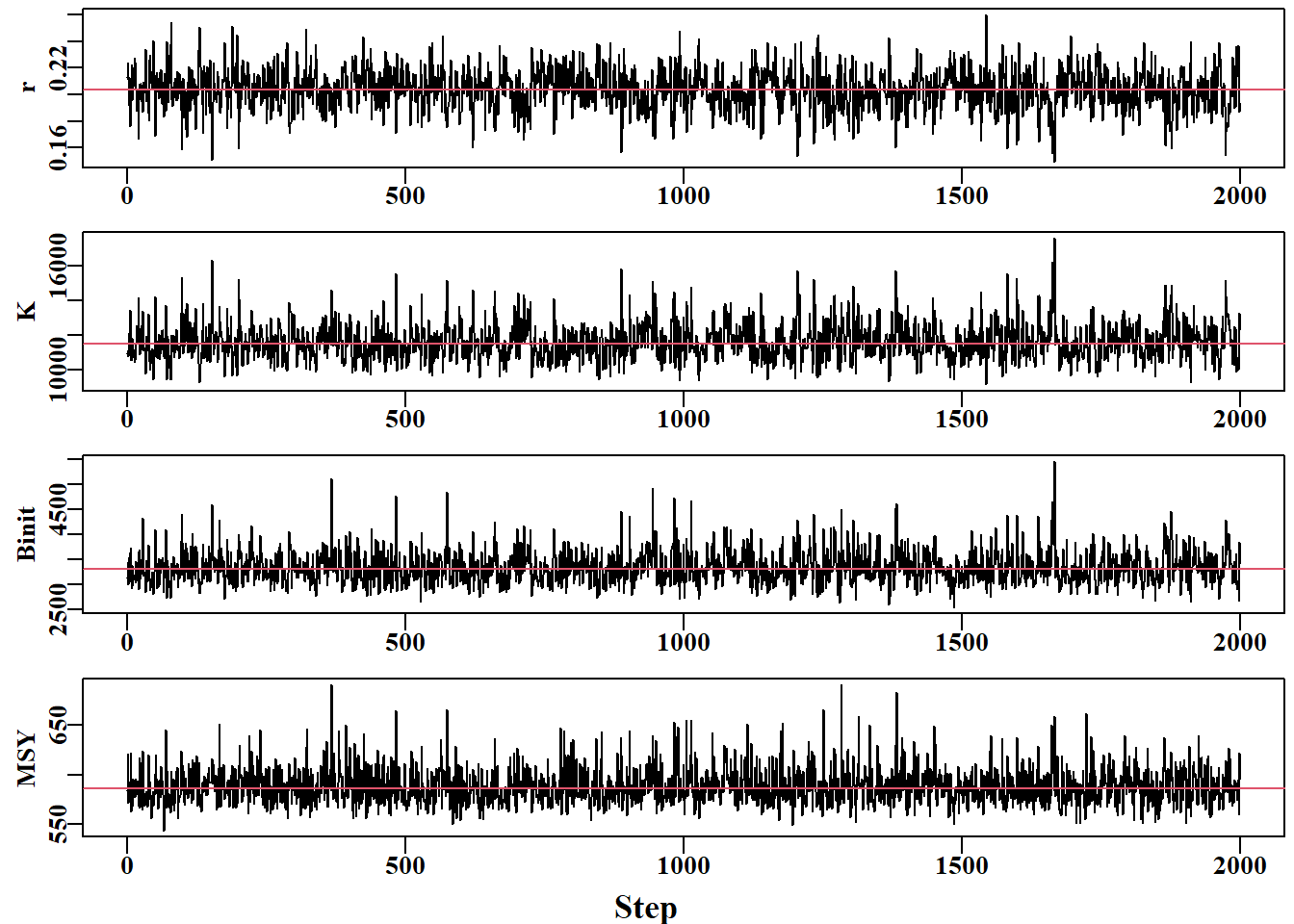

#Traces for the Fox model parameters from the MCMC Fig7.26 parset(plots=c(4,1),margin=c(0.3,0.45,0.05,0.05), outmargin =c(1,0,0,0),cex=0.85)label<-colnames(post1)N<-dim(post1)[1]for(iin1:3){plot(1:N,post1[,i],type="l",lwd=1,ylab=label[i],xlab="")abline(h=median(post1[,i]),col=2)}msy<-post1[,1]*post1[,2]/4plot(1:N,msy,type="l",lwd=1,ylab="MSY",xlab="")abline(h=median(msy),col=2)mtext("Step",side=1,outer=T,line=0.0,font=7,cex=1.1)

三个主要 Schaefer 模型参数和 MSY 估计值的迹线。如果细化步长增加到 1024 步或更长,迹线内剩余的自相关性应得到改善。The traces for the three main Schaefer model parameters and the MSY estimates. The remaining auto-correlation within traces should be improved if the thinning step were increased to 1024 or longer.

#Do five chains of the same length for the Fox model set.seed(6396679)# Note all chains start from same place, which is inscale<-c(0.07,0.05,0.09,0.45)# suboptimal, but still the chains pars<-log(c(r=0.205,K=11300,Binit=3220,sigma=0.044))# differ result<-do_MCMC(chains=5,burnin=50,N=2000,thinstep=512, inpar=pars,infunk=negLL1,calcpred=simpspmC, obsdat=log(fish[,"cpue"]),calcdat=fish, priorcalc=calcprior,scales=inscale, schaefer=FALSE)cat("acceptance rate = ",result$arate," \n")# always check this

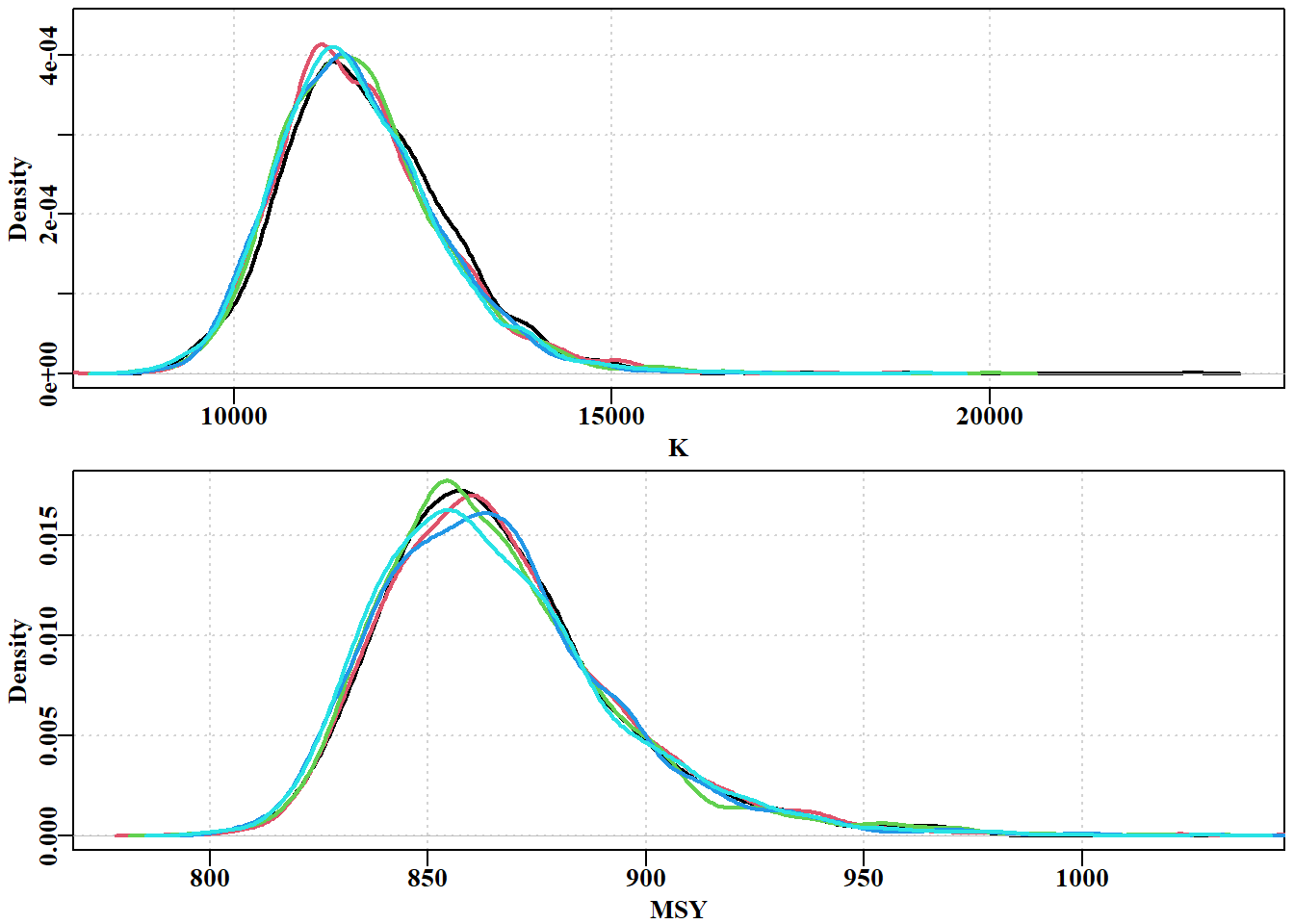

#Now plot marginal posteriors from 5 Fox model chains Fig7.27 parset(plots=c(2,1),cex=0.85,margin=c(0.4,0.4,0.05,0.05))post<-result[[1]][[1]]plot(density(post[,"K"]),lwd=2,col=1,main="",xlab="K", ylim=c(0,4.4e-04),panel.first=grid())for(iin2:5)lines(density(result$result[[i]][,"K"]),lwd=2,col=i)p<-1e-08post<-result$result[[1]]msy<-post[,"r"]*post[,"K"]/((p+1)^((p+1)/p))plot(density(msy),lwd=2,col=1,main="",xlab="MSY",type="l", ylim=c(0,0.0175),panel.first=grid())for(iin2:5){post<-result$result[[i]]msy<-post[,"r"]*post[,"K"]/((p+1)^((p+1)/p))lines(density(msy),lwd=2,col=i)}

图 7.26: K 参数的边际后验值和 5 链 2000 次重复(512 * 2000 = 1049600 次迭代)得出的隐含 MSY。分布之间仍存在一些差异,尤其是在模式处,这表明更多的重复和更高的稀疏率可能会改善结果。the marginal posterior for the K parameter and the implied MSY from five chains of 2000 replicates (512 * 2000 = 1049600 iterations). Some variation remains between the distributions, especially at the mode, suggesting that more replicates and potentially a higher thinning rate would improve the outcome.

# get qunatiles of each chain probs<-c(0.025,0.05,0.5,0.95,0.975)storeQ<-matrix(0,nrow=6,ncol=5,dimnames=list(1:6,probs))for(iin1:5)storeQ[i,]<-quants(result$result[[i]][,"K"])x<-apply(storeQ[1:5,],2,range)storeQ[6,]<-100*(x[2,]-x[1,])/x[2,]

表 7.8: 针对 abdat 数据的 Fox 模型运行的五条 MCMC 链中 K 参数的五个量化值。最后一行是各链数值范围的百分比差异,显示它们的中位数相差略高于 1%。Five quantiles on the K parameter from the five MCMC chains run on the Fox model applied to the abdat data. The last row is the percent difference in the range of the values across the chains, which shows their medians differ by slightly more than 1%.

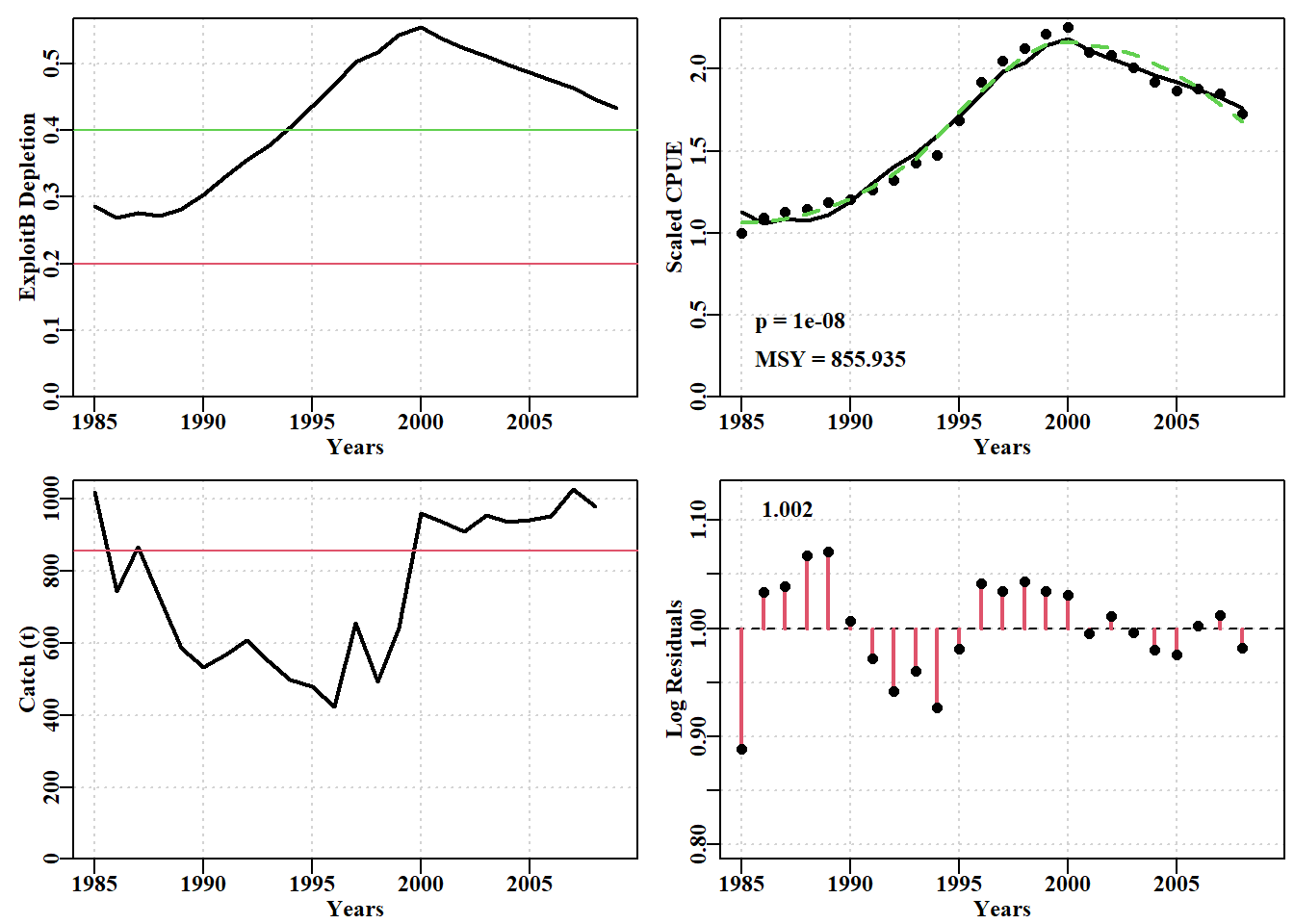

#Prepare Fox model on abdat data for future projections Fig7.28 data(abdat); fish<-as.matrix(abdat)param<-log(c(r=0.3,K=11500,Binit=3300,sigma=0.05))bestmod<-nlm(f=negLL1,p=param,funk=simpspm,schaefer=FALSE, logobs=log(fish[,"cpue"]),indat=fish,hessian=TRUE)optpar<-exp(bestmod$estimate)ans<-plotspmmod(inp=bestmod$estimate,indat=fish,schaefer=FALSE, target=0.4,addrmse=TRUE, plotprod=FALSE)

图 7.27: 使用 Fox 模型和对数正态误差拟合的 abdat 数据集最佳模型。绿色虚线为黄土曲线,红色实线为最佳预测拟合模型。请注意对数正态残差的模式,这表明该模型在该数据方面存在一些不足。The optimum model fit for the abdat data-set using the Fox model and log-normal errors. The green dashed line is a loess curve while the solid red line is the optimum predicted model fit. Note the pattern in the log-normal residuals indicating that the model has some inadequacies with regard to this data.

表 7.9: 前十行为 abdat 数据集所代表的种群动态预测值和最佳 Fox 模型拟合值。The first ten rows of the predicted dynamics of the stock represented by the abdat data-set and the optimal Fox model fit.

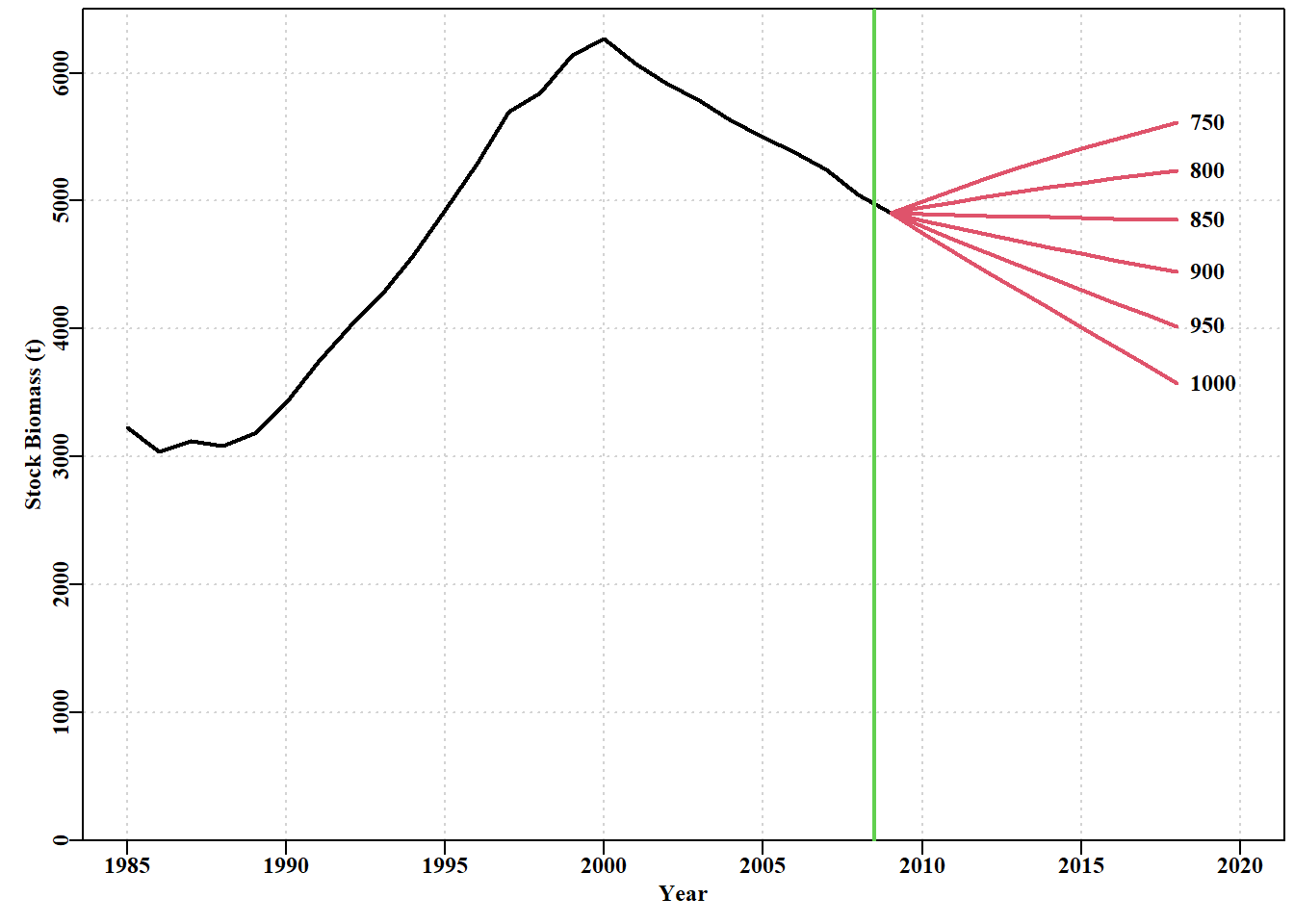

# Fig 7.29 catches<-seq(700,1000,50)# projyr=10 is the default projans<-spmprojDet(spmobj=out,projcatch=catches,plotout=TRUE)

图 7.28: 根据 abdat 数据集拟合的最佳 Fox 模型的确定性恒定渔获量预测。垂直绿线是可用数据的极限,其右侧的红线是主要预测。数字是施加的恒定渔获量。Deterministic constant catch projections of the optimum Fox model fit to the abdat data-set. the vertical green line is the limit of the data available and the red lines to the right of that are the main projections. The numbers are the constant catches imposed.

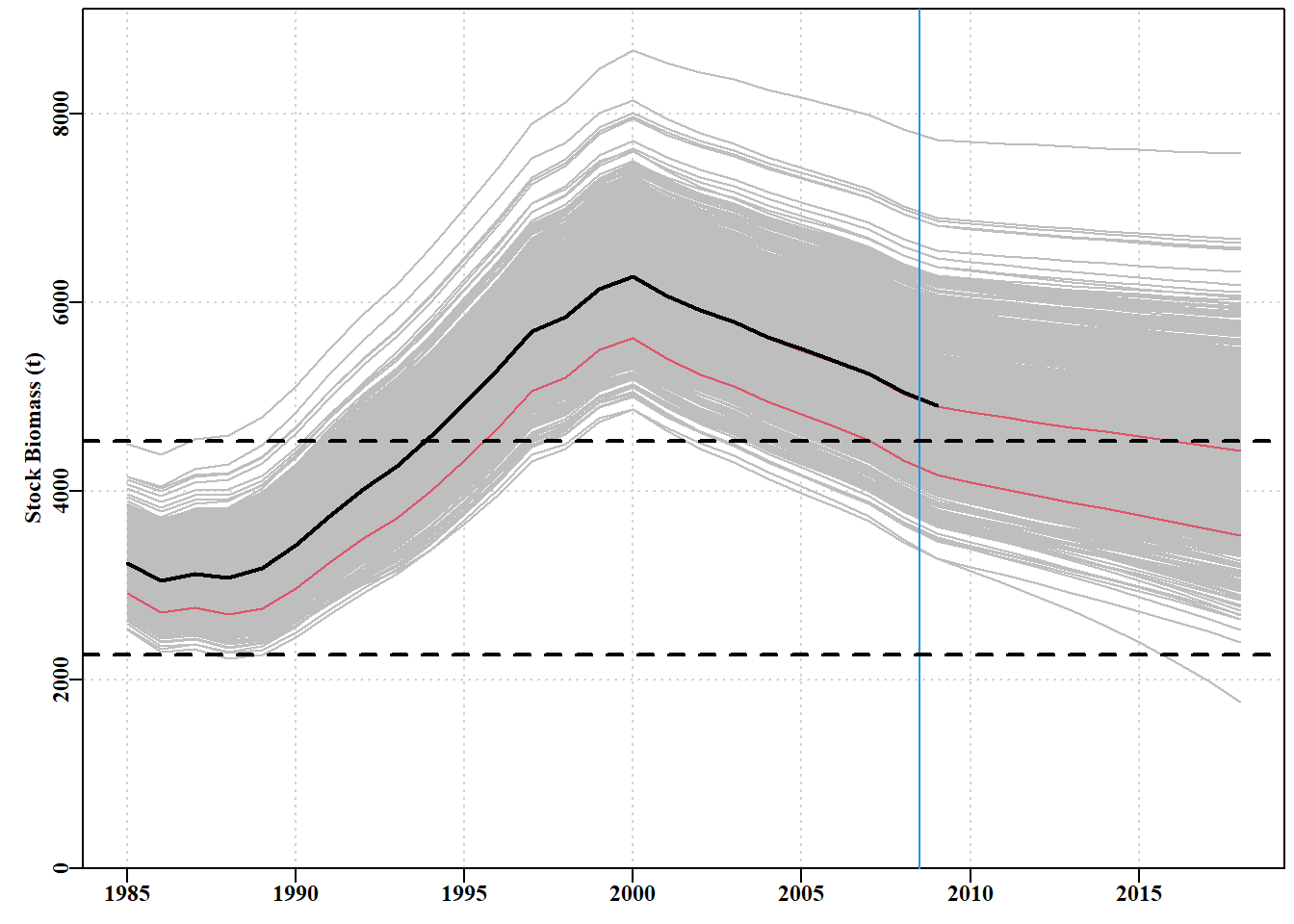

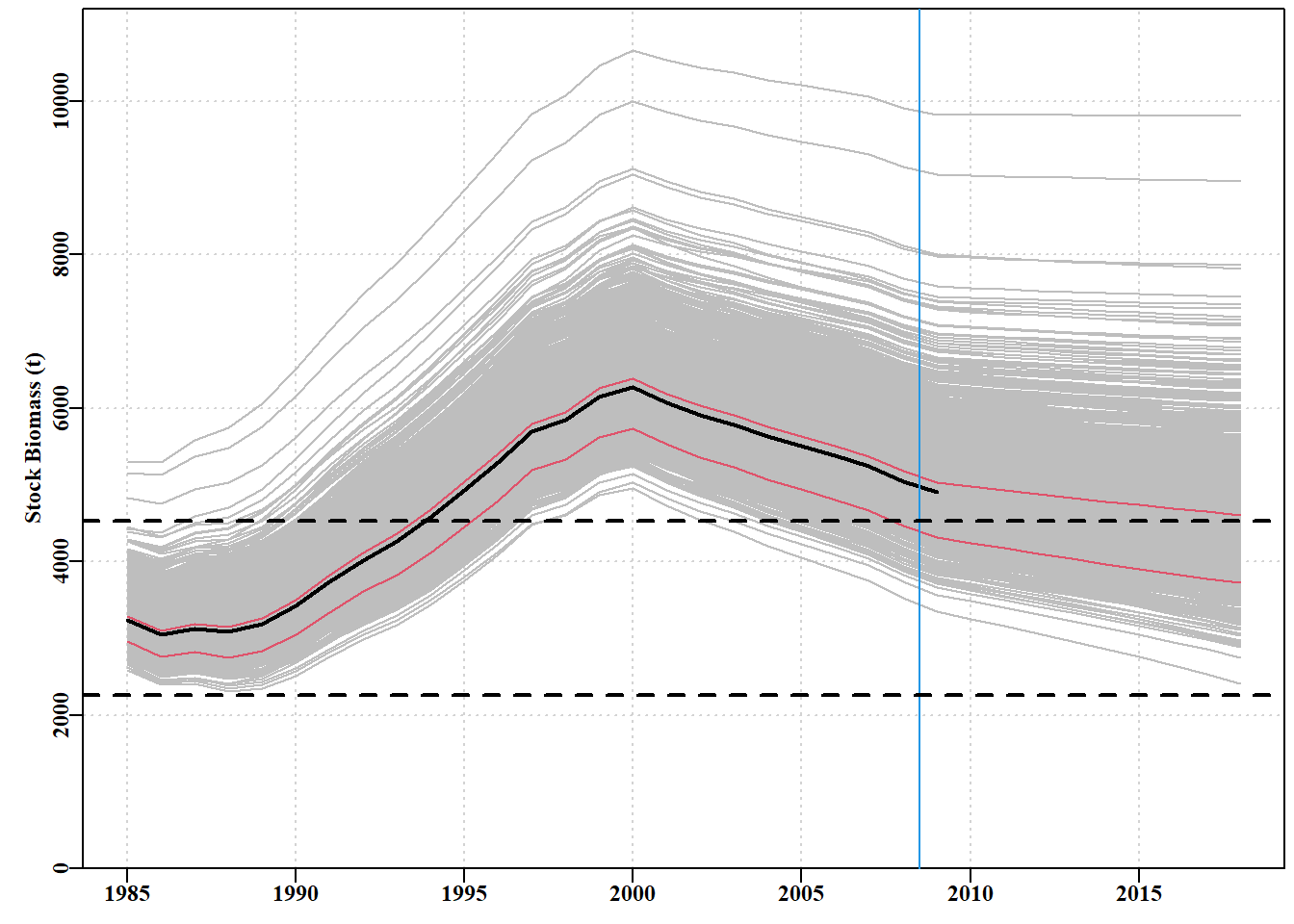

# generate parameter vectors from a multivariate normal # project dynamics under a constant catch of 900t library(mvtnorm)matpar<-parasympt(bestmod,N=1000)#generate parameter vectors projs<-spmproj(matpar,fish,projyr=10,constC=900)#do dynamics

图 7.29: 1000 个预测值,通过使用反向哈希值和平均参数估计值生成 1000 个可信参数向量,并将每 个向量与 10 年不变的 900 吨渔获量后的渔获量向前推算得出。虚线为极限和目标参考点。蓝色垂直线是渔业数据的极限,黑色粗线是最优拟合,与最优线平行的红色细线是各年的第 10 和第 50 个量值。1000 projections derived from the using the inverse hessian and mean parameter estimates to generate 1000 plausible parameter vectors and projecting each vector forward with the fisheries catches followed by 10 years of a constant catch of 900t. The dashed lines are the limit and target reference points. The blue vertical line is the limit of fisheries data, the thick black line is the optimum fit and the thin red lines parallel to the optimum line are the 10th and 50th quantiles across years.

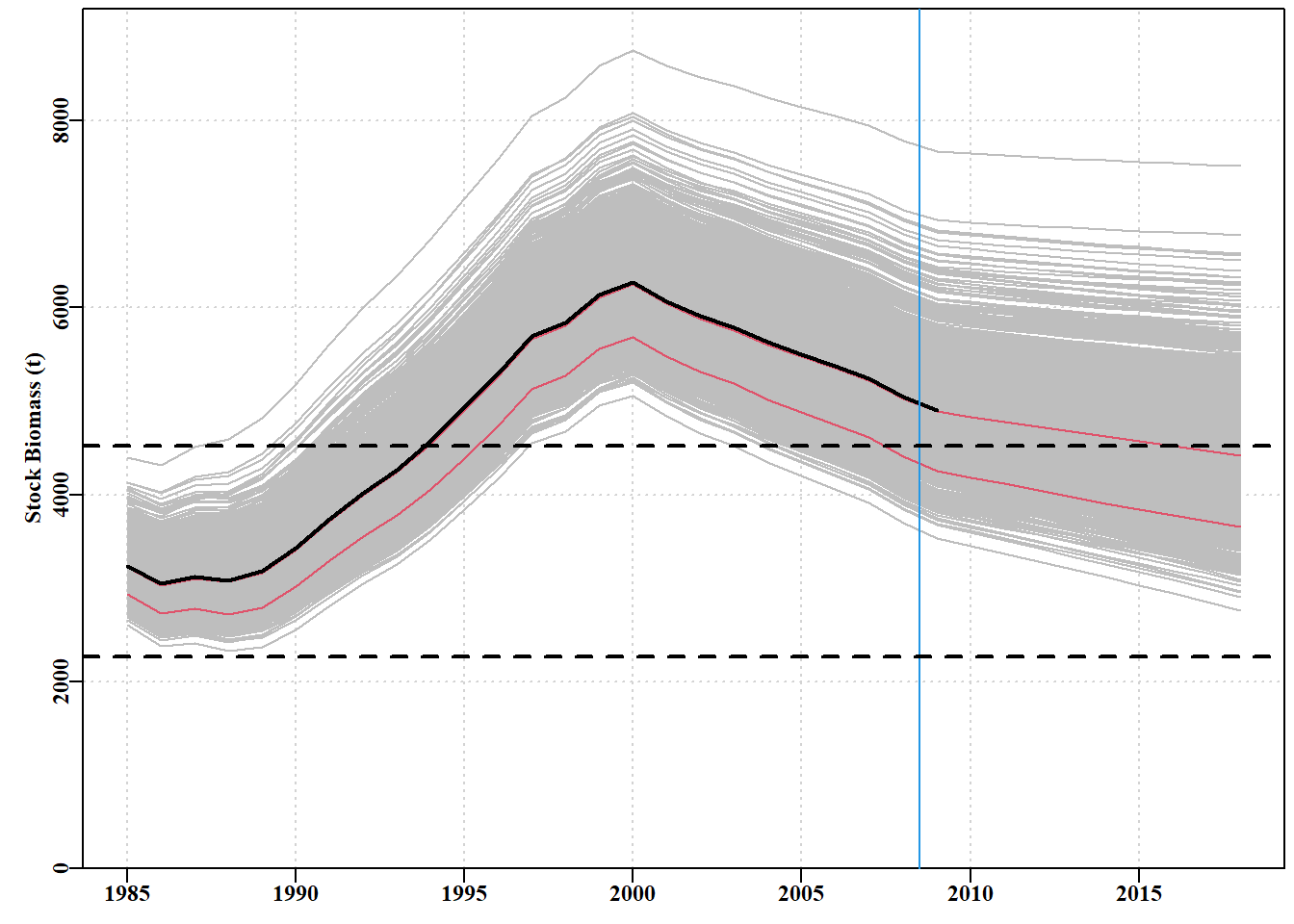

#bootstrap generation of plausible parameter vectors for Fox reps<-1000boots<-spmboot(bestmod$estimate,fishery=fish,iter=reps, schaefer=FALSE)matparb<-boots$bootpar[,1:4]#examine using head(matparb,20)

#bootstrap projections. Lower case b for boostrap Fig7.31 projb<-spmproj(matparb,fish,projyr=10,constC=900)outb<-plotproj(projb,out,qprob=c(0.1,0.5),refpts=c(0.2,0.4))

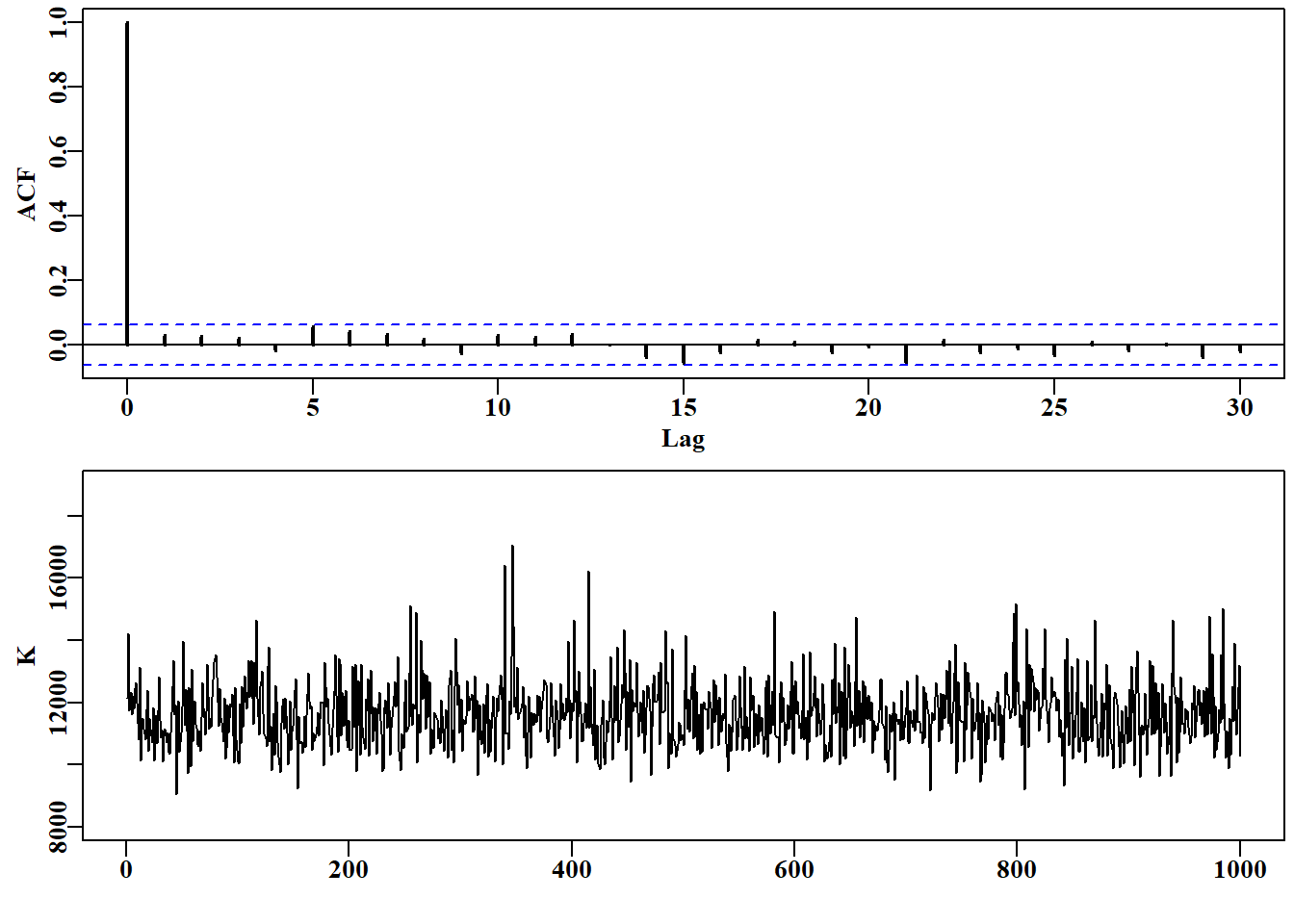

# auto-correlation, or lack of, and the K trace Fig 7.32 parset(plots=c(2,1),cex=0.85)acf(parB[,2],lwd=2)plot(1:N,parB[,2],type="l",ylab="K",ylim=c(8000,19000),xlab="")

图 7.31: 从上图可以明显看出,过剩产量模型福克斯版本的 K 参数后验分布的 1000 次抽样中缺乏自相关性。下图中的迹线显示了典型的分散值,但保留了一些更极端的峰值。

# Fig 7.33 matparB<-as.matrix(parB[,1:4])# B for Bayesian projs<-spmproj(matparB,fish,constC=900,projyr=10)# project them plotproj(projs,out,qprob=c(0.1,0.5),refpts=c(0.2,0.4))#projections

在贝叶斯分析中,我们希望使用 Fox 剩余产量模型。这当然可以使用函数 simpspm(),通过修改 schaefer 参数来实现。但是

代码

library(Rcpp)cppFunction('NumericVector simpspmC(NumericVector pars, NumericMatrix indat, LogicalVector schaefer) { int nyrs = indat.nrow(); NumericVector predce(nyrs); NumericVector biom(nyrs+1); double Bt, qval; double sumq = 0.0; double p = 0.00000001; if (schaefer(0) == TRUE) { p = 1.0; } NumericVector ep = exp(pars); biom[0] = ep[2]; for (int i = 0; i < nyrs; i++) { Bt = biom[i]; biom[(i+1)] = Bt + (ep[0]/p)*Bt*(1 - pow((Bt/ep[1]),p)) - indat(i,1); if (biom[(i+1)] < 40.0) biom[(i+1)] = 40.0; sumq += log(indat(i,2)/biom[i]); } qval = exp(sumq/nyrs); for (int i = 0; i < nyrs; i++) { predce[i] = log(biom[i] * qval); } return predce; }')

Elder, R. D. 1979. 《Equilibrium Yield for the Hauraki Gulf Snapper Fishery Estimated from Catch and Effort Figures, 196074》. New Zealand Journal of Marine and Freshwater Research 13 (1): 31–38. https://doi.org/10.1080/00288330.1979.9515778.

Hilborn, Ray. 1979. 《Comparison of Fisheries Control Systems That Utilize Catch and Effort Data》. Journal of the Fisheries Research Board of Canada 36 (12): 1477–89. https://doi.org/10.1139/f79-215.

MacCall, Alec D. 2009. 《Depletion-Corrected Average Catch: A Simple Formula for Estimating Sustainable Yields in Data-Poor Situations》. ICES Journal of Marine Science 66 (10): 2267–71. https://doi.org/10.1093/icesjms/fsp209.

Polacheck, Tom, Ray Hilborn, 和 Andre E. Punt. 1993. 《Fitting Surplus Production Models: Comparing Methods and Measuring Uncertainty》. Canadian Journal of Fisheries and Aquatic Sciences 50 (12): 2597–607. https://doi.org/10.1139/f93-284.

Prager, Michael. 1994. 《A suite of extensions to a nonequilibrium surplus-production model》. Fishery Bulletin 92 (一月): 374–89.

Punt, Andre E., 和 Ray Hilborn. 1997. 《Fisheries Stock Assessment and Decision Analysis: The Bayesian Approach》. Reviews in Fish Biology and Fisheries 7 (1): 35–63. https://doi.org/10.1023/A:1018419207494.

Saila, S. B., J. H. Annala, J. L. McKoy, 和 J. D. Booth. 1979. 《Application of Yield Models to the New Zealand Rock Lobster Fishery》. New Zealand Journal of Marine and Freshwater Research 13 (1): 1–11. https://doi.org/10.1080/00288330.1979.9515775.

Schaefer, M. 1991. 《Some Aspects of the Dynamics of Populations Important to the Management of the Commercial Marine Fisheries》. Bulletin of Mathematical Biology 53 (1-2): 253–79. https://doi.org/10.1016/s0092-8240(05)80049-7.

Winker, Henning, Felipe Carvalho, 和 Maia Kapur. 2018. 《JABBA: Just Another Bayesian Biomass Assessment》. Fisheries Research 204 (八月): 275–88. https://doi.org/10.1016/j.fishres.2018.03.010.

源代码